10-K: Annual report pursuant to Section 13 and 15(d)

Published on March 15, 2013

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2012

Commission File Number 0-21886

BARRETT BUSINESS SERVICES, INC.

(Exact name of registrant as specified in its charter)

| Maryland | 52-0812977 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

|

| 8100 NE Parkway Drive, Suite 200 Vancouver, Washington |

98662 | |

| (Address of principal executive offices) | (Zip Code) | |

(360) 828-0700

(Registrants telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered |

|

| Common Stock, Par Value $0.01 Per Share |

The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrants knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company (as indicated by Exchange Act Rule 12b-2).

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

State the aggregate market value of the common equity held by non-affiliates of the registrant: $144,678,000 at June 30, 2012

Indicate the number of shares outstanding of each of the registrants classes of common stock, as of the latest practicable date:

| Class |

Outstanding at March 1, 2013 |

|

| Common Stock, Par Value $.01 Per Share | 7,022,109 Shares |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for the 2013 Annual Meeting of Stockholders are hereby incorporated by reference into Part III of Form 10-K.

Table of Contents

BARRETT BUSINESS SERVICES, INC.

2012 ANNUAL REPORT ON FORM 10-K

- 1 -

Table of Contents

| Item 1. | BUSINESS |

General

Barrett Business Services, Inc. (BBSI, the Company, our or we), was incorporated in the state of Maryland in 1965. We are a leading provider of business management solutions, combining human resource outsourcing and professional management consulting to create an operational platform that differentiates us from our competitors. Our integrated platform is grounded in expertise in payroll processing, employee benefits, workers compensation coverage, risk management and workplace safety programs, human resource administration, recruiting and permanent placement. BBSI helps small-to medium-sized businesses improve the efficiency of their operations. Our principal services assist our clients in leveraging their investment in human capital. We believe that our combination of business management solutions and expertise in human capital management enables us to provide our clients with a unique blend of services not offered by our competitors.

Our focus is to become the leading provider of business management solutions for small and medium-sized businesses in the markets we serve. We seek to differentiate ourselves by offering a comprehensive suite of professional support services delivered by operations-focused personnel at branch offices located in close proximity to our client operations. We believe that the high-touch nature of our business model, combined with the integrated nature of our service platform, assists our clients in successfully aligning and strengthening their organizational structure to meet the demands of their businesses.

We promote a decentralized and autonomous management structure by hiring senior-level managers to oversee, develop and expand our business at the branch-office level. We recruit highly experienced senior-level area managers who possess the skill set to handle the day-to-day demands of our business, focus on business development and be proactive in addressing client needs. We believe that making significant investments in the best management talent available, within their respective areas of expertise, will enable us to leverage the value of this investment many times over.

We motivate our management employees through a compensation package that includes a competitive base salary structure at the branch-office level and provides the opportunity to earn additional profit sharing on a quarterly basis. Each branch-level employee has the opportunity to earn profit sharing based upon branch office profitability above minimum thresholds. Our internal risk consultants have an opportunity to earn incentive compensation based upon the workers compensation claims experience of their specific client base.

We control workers compensation costs through a cultural foundation of risk mitigation and workplace safety. We employ a rigorous underwriting process to assess financial stability, risk factors, and cultural alignment related to safety and continuous improvement in the workplace. Our senior leadership is actively involved in the underwriting process, which begins with the careful selection of potential client companies. If the candidate company satisfies all underwriting standards, we accept the company. If a clients safe-work culture or adherence to workplace safety procedures declines to unsatisfactory levels, we will terminate the relationship, consistent with applicable contract terms.

- 2 -

Table of Contents

As of December 31, 2012, we have clients with employees located in 23 states and the District of Columbia, through a network of 50 branch locations in California, Oregon, Washington, Idaho, Arizona, Utah, Colorado, Maryland, Delaware and North Carolina. We also have several smaller recruiting locations in our general market areas, which are under the direction of a branch office.

Our expansion strategy is based primarily on organic, location-driven growth in the markets in which we currently do business. Since our initial public offering in June 1993, we have also completed 27 acquisitions of complementary businesses. In order to increase our client base, expand our presence in existing markets, enter new markets and broaden our service offerings, we may pursue additional strategic acquisitions, but there is no assurance that we will complete such transactions.

Categories of Services

We report financial results in two categories of services: Professional Employer Services (PEO) and Staffing. During 2012, we served approximately 2,910 PEO clients, which compares to approximately 2,355 PEO clients during 2012. In addition, at December 31, 2012, we served approximately 2,550 PEO clients and employed approximately 56,210 employees pursuant to PEO contracts, as compared to approximately 1,935 PEO clients and approximately 41,500 employees as of December 31, 2011. During 2012, we provided staffing services to approximately 1,850 staffing services customers, which compares to approximately 1,815 customers during 2011. See the table on page 29 of this report for the percentages of total net revenues from our staffing and PEO services for the three years in the period ended December 31, 2012.

PEO. We enter into a client services agreement to become a co-employer of the clients existing workforce, assuming responsibility for payroll, payroll taxes, workers compensation coverage and certain other administration functions, while the business owner client maintains physical care, custody and control of their workforce, including the authority to hire and terminate employees.

We have client services agreements with a diverse array of customers, including among others, electronics manufacturers, various light-manufacturing industries, agriculture-based companies, transportation and shipping enterprises, food processing, telecommunications, public utilities, general contractors in various construction-related fields and professional services firms.

Staffing and Recruiting. Through our deep network of professionals and our expertise in recruiting, we are able to identify and source the right talent to meet the needs of our clients. Through our assessment process, we gain an understanding of short and long term needs of our clients, allowing us to identify the right talent for each position. We then conduct a rigorous screening process to help ensure a successful hire.

Our staffing services include on-demand or short-term staffing assignments, contract staffing, long-term or indefinite-term on-site management, and direct placement. As more and more companies focus on effectively managing variable costs and reducing fixed overhead, the use of employees on a short-term basis allows firms to utilize the just-in-time approach for their personnel needs, thereby converting a portion of their fixed personnel costs to a variable expense.

- 3 -

Table of Contents

Our staffing employees are not under our direct control while working at a customers business. While we have not experienced any significant liability due to claims arising out of negligent acts or misconduct by our staffing services employees, claims could be asserted against us which could have a material adverse effect on our financial condition and results of operations.

In 2012, the light-industrial sector generated approximately 85% of our staffing services revenues, while clerical office staff accounted for 11% of such revenues and technical personnel represented the balance of 4%. Our light-industrial workers perform such tasks as operation of machinery, manufacturing, loading and shipping, site preparation for special events, construction-site cleanup and janitorial services. Technical personnel include electronic parts assembly workers and designers of electronic parts.

Our Services

Our passage from an entrepreneurially run company to a professionally managed organization has helped to form our view that all businesses experience the same success factors in their growth, as well as the same potential pitfalls. The insights gained through our own growth, along with the trends we see in working with more than 3,000 companies each day, define our approach to guiding business owners through the challenges associated with being an employer.

We believe the expert knowledge of our teams combined with tools from the HR outsourcing industry helps our clients more effectively leverage their internal resources. We assist our clients by:

| | Partnering with the business owner to frame a three-tiered management platform that brings predictability to their organization |

| | Leveraging our clients investment in human capital through a unique, high-touch, results-oriented approach |

| | Enabling business owners to focus on their core business by reducing organizational complexity and maximizing productivity |

Prior to entering into a client services agreement, we perform an in-depth analysis of the potential clients operations, including evaluation of needs and objectives, risk assessment and financial review. Once the client service agreement has been signed, we pair each of our clients with a dedicated, local branch-based business unit comprised of management professionals with expertise in Human Resource Consulting, Risk Consulting, Payroll, Benefits Administration and Recruiting. We believe our hands-on model allows our clients to more quickly adopt processes to develop a more productive workforce, mitigate workplace injury and risk and encourage workplace compliance with a broad range of employment and safety regulations.

- 4 -

Table of Contents

Our three-tiered management platform has clients following a structured progression:

Tier 1: Tactical Alignment

The first stage, which includes an implementation process, addresses the administrative and tactical components of managing employees, while aligning the business owners culture with BBSIs processes, controls and culture.

Tier 2: Supervisor Development

The second stage of the relationship focuses on continuing process improvement, further development of best practices, supervisor development and leadership training.

Tier 3: Business-level guidance

Activities involved in the third stage of the relationship are more strategic and forward-looking with a goal of cultivating an environment in the clients organization in which employees and supervisors, instead of the business owner, drive the success of the organization.

We have the ability to provide workers compensation coverage as a means of meeting statutory requirements and protecting our clients from employment-related injury claims. Through our internal claims managers and our third-party administrators, we provide claims management services for our co-employed clients. We work aggressively to manage and reduce job injury claims, including identifying fraudulent claims and requiring our client companies to offer modified duty to their employees.

We assist our clients in retaining the best employees for their businesses by helping them obtain, at their cost, comprehensive health benefits, including medical, dental and vision benefits, life and accident insurance, and short-term and long-term disability coverage. We also provide, without separate administrative fees, a 401(k) retirement savings plan and a Section 125 cafeteria plan.

Clients and Client Contracts

Our business is typically characterized by long-term relationships that result in recurring revenue. Our annual retention rate is in excess of 90%. We do periodically terminate clients who no longer meet our risk or financial criteria. We do not include those terminated clients in our retention count.

None of our co-employed clients or our staffing services customers individually represented more than 1% of our total revenues in 2012.

Our standard client services agreement typically provides for an initial term of one year with automatic renewal for one-year periods. Our agreements generally permit cancellation by either party upon 30 days written notice. In addition, we may terminate the agreement at any time for specified reasons, including nonpayment or failure to follow our workplace safety program.

The client services agreement also provides for indemnification of us by the client against losses arising out of any default by the client under the agreement, including failure to comply with any employment-related, health and safety, or immigration laws or regulations.

- 5 -

Table of Contents

We require our co-employed clients to maintain comprehensive liability coverage in the amount of $1.0 million for acts of our work-site employees. Although no claims exceeding such policy limits have been paid by us to date, the possibility exists that claims for amounts in excess of sums available to us through indemnification or insurance may be asserted in the future, which could adversely affect profitability.

Market Opportunity

The human resource outsourcing industry is large and continuing to expand, particularly among small-to mid-sized businesses. Some of the key factors driving our growth include the desire of businesses to outsource non-core business functions, to reduce regulatory risk in an increasingly complex employment landscape, to mitigate costs and complexity associated with workers compensation coverage, and to maximize their investment in human capital. We believe our ability to combine our experience in human capital management with the knowledge-based approach of the business consulting industry has enabled us to capitalize on the trend toward increased human resource outsourcing.

We believe the small and medium-sized business segment is particularly attractive because:

| | this segment is large and has a low penetration rate by providers of outsourced comprehensive human resource services; |

| | small and medium-sized businesses typically have fewer in-house resources than larger businesses and, as a result, are generally more dependent on service providers; |

| | quality of service, ease-of-use and responsiveness to clients needs are key considerations of this business segment in selecting a service provider; |

| | this segment is generally characterized by a relatively high client retention rate and lower client acquisition costs. |

Competition

The business environment in which we operate is characterized by intense competition and fragmentation. BBSI is not aware of reliable statistics regarding the number of its competitors, but certain large, well-known companies typically compete with us in the same markets and also have greater financial and marketing resources than we do, including Automatic Data Processing, Inc., Manpower, Inc., Kelly Services, Inc., Insperity, Inc., TriNet, and Paychex, Inc., among others. We may face additional competition in the future from new entrants to the field, including other staffing services companies, payroll processing companies and insurance companies. The principal competitive factors in the business environment in which we operate are price and level of service.

We believe that our past growth is attributable to our ability to provide small and medium-sized companies with the resources and knowledge base of a large employer delivered through a local operations team. We help clients to reduce workers compensation costs and bring stability to their business through our hands-on risk mitigation model. We believe our level of integration with each client business provides a competitive advantage.

- 6 -

Table of Contents

Our competitive advantage may be adversely affected by a substantial increase in the costs of maintaining our self-insured workers compensation program, or changes in the regulatory environment, particularly in California.

Sales and Marketing

Our area managers and a team of business development professionals lead the sales and marketing effort for BBSI. Business development is the primary function of our area managers, and is focused on branch-level development of local business relationships. We believe our clients are our best advocates and powerful drivers of our brand awareness. We support our clients and foster advocacy through branch-based business units. The business unit is an integrated team comprised of an internal Client Business Partner, HR Consultant, Risk Consultant and a Payroll Specialist. By adding branch business units in the markets in which we already do business, we expect to see incremental growth driven by our reputation and client referrals.

On a regional and national level, we seek to expand and align our services to meet business demand, which may include opening additional offices to better support a clients geographic needs, or adding new business units within an existing branch location.

To supplement the sales efforts of our area managers, we rely on an extensive network of referral partners. Our referral partners include insurance brokers, CPAs, and other business professionals who can facilitate an introduction to prospective clients. These partners, in exchange for a fee equivalent to a small percentage of payroll, facilitate introductions to business owners on our behalf.

Growth Strategy

Our growth strategy is supported by our focus in the following areas:

| | Support, strengthen and expand branch office operations. We believe that strengthening and expanding the operations of each location is an efficient and effective means of increasing market share in the geographic areas in which we do business. Our primary means of adding capacity is through the creation of business units within each branch. The business unit, an integrated team comprised of an internal client Business Partner, HR Consultant, a Risk Consultant and a Payroll Specialist provide tactical and strategic guidance to our client base. As our presence in each market grows through the addition of branch business units, we believe market awareness of our reputation and services increases. |

| | Increase client utilization of our services. We believe that we will be able to continue to maintain our average level of margin and improve client retention as our clients more fully utilize our current service offerings. We invest substantial time integrating our services into our client organizations to optimize their effectiveness and measure their results. Our long-term partnership philosophy provides us with the opportunity to expand our range of services to a given client. |

| | Enhance management information systems. We continue to invest in developing our information technology infrastructure. We believe that our platform gives us a competitive advantage by allowing us to provide a high level of flexibility to satisfy a |

- 7 -

Table of Contents

| variety of demands of our small and medium-sized business clients on a cost-effective basis. Furthermore, we believe that our current technology platform is capable of supporting our planned development of new business units for the foreseeable future. |

| | Penetrate new markets. We intend to open additional branch offices in new geographic markets as opportunities arise. We have developed a well-defined approach to geographic expansion, which will serve as a guide for entering new markets. |

| | Pursue strategic acquisitions. We have completed 27 acquisitions since our initial public offering in June 1993. Our acquisition targets are typically staffing companies. We have acquired companies in the PEO industry less frequently because they typically do not align with our risk mitigation model and our overall culture. Because our operations are focused primarily in the western third of the United States, future acquisitions, if any, will likely focus on expanding our geographic footprint into contiguous regions. There can be no assurance, however, that any additional acquisitions will be completed in the future. |

Self-Insured Workers Compensation Program

A principal service we provide to our customers, particularly our PEO clients, is workers compensation coverage. Through our co-employment agreements, we are responsible for complying with applicable statutory requirements for workers compensation coverage. Our workplace safety services are closely tied to our approach to the management of workers compensation risk.

Elements of Workers Compensation System. State law (and for certain types of employees, federal law) generally mandates that an employer reimburse its employees for the costs of medical care and other specified benefits for injuries or illnesses, including catastrophic injuries and fatalities, incurred in the course and scope of employment. The benefits payable for various categories of claims are determined by state regulation and vary with the severity and nature of the injury or illness and other specified factors. In return for this guaranteed protection, workers compensation is an exclusive remedy and employees are generally precluded from seeking other damages from their employer for workplace injuries. Most states require employers to maintain workers compensation insurance or otherwise demonstrate financial responsibility to meet workers compensation obligations to employees. In many states, employers who meet certain financial and other requirements are permitted to self-insure. See Regulatory and Legislative Issues below for a discussion of recent developments in California.

Self Insurance for Workers Compensation. In August 1987, we became a self-insured employer for workers compensation coverage in Oregon. We subsequently obtained self-insured employer status for workers compensation in four additional states, California, Delaware, Maryland and Colorado, as well as in Washington for our staffing and management employees. Regulations governing self-insured employers in each jurisdiction typically require the employer to maintain surety deposits of government securities, letters of credit or other financial instruments to cover workers claims in the event the employer is unable to pay for such claims.

- 8 -

Table of Contents

To manage our financial exposure from the incidence of catastrophic injuries and fatalities, we maintain excess workers compensation insurance coverage. We maintain a wholly owned, fully licensed captive insurance company incorporated in Arizona, Associated Insurance Company for Excess (AICE), to provide us with excess workers compensation coverage from $1.0 million up to $5.0 million per occurrence in the states of Oregon, California, Delaware and Washington. Additional excess workers compensation insurance coverage is provided through annual policies issued by ACE American Insurance Company from $5.0 million to $15.0 million per occurrence, except for our Maryland and Colorado operations. Our excess insurance policy in Maryland has a $1.0 million retention with a $25.0 million limit and our excess insurance policy in Colorado has a $500,000 retention and statutory limits on a per occurrence basis. This approach results in an effective per occurrence retention, on a consolidated basis, of $5.0 million. This higher per occurrence retention may result in higher workers compensation costs to us with a corresponding negative effect on our operating results. AICE provides us with access to an alternative mechanism for excess insurance coverage, as well as certain income tax benefits arising from the ability to accelerate the deduction, for tax purposes, of certain accruals for workers compensation claims.

Effective January 5, 2010, we formed Ecole Insurance Company, a wholly owned fully licensed insurance company in Arizona (Ecole), to provide workers compensation coverage to our employees working in Arizona, beginning with claims occurring on or after March 1, 2010. Additional excess workers compensation insurance coverage for Ecole is provided by a major insurance company from $1.0 million to statutory limits per occurrence. As discussed in Liquidity and Capital Resources in Item 7, we are considering expanding Ecoles geographic reach to California.

Claims Management. As a self-insured employer, our workers compensation expense is tied directly to the incidence and severity of workplace injuries to our employees. We seek to contain our workers compensation costs through an aggressive approach to claims management. We use managed-care systems to reduce medical costs and keep time-loss costs to a minimum by assigning injured workers, whenever possible, to short-term assignments which accommodate the workers physical limitations. We believe that these assignments minimize both time actually lost from work and covered time-loss costs. We employ internal, professionally licensed claims adjusters and engage third-party claims administrators (TPAs) to provide the principal claims management expertise. Typical management procedures include performing thorough and prompt on-site investigations of claims filed by employees, working with physicians to encourage efficient medical management of cases, denying questionable claims and attempting to negotiate early settlements to eliminate future development of claims costs. We also maintain a corporate-wide pre-employment drug screening program and a mandatory post-injury drug test. The program is believed to have resulted in a reduction in the frequency of fraudulent claims and in accidents in which the use of illegal drugs appears to have been a contributing factor.

Elements of Self-Insurance Costs. The costs associated with our self-insured workers compensation program include case reserves for reported claims, an additional expense provision for potential future increases in the cost of open injury claims (known as adverse loss development) and claims incurred in prior periods but not reported (referred to as IBNR), fees payable to our TPAs, additional claims administration expenses,

- 9 -

Table of Contents

administrative fees payable to state workers compensation regulatory agencies, legal fees, broker commissions for business referrals, premiums for excess workers compensation insurance, and costs associated with forming and operating our wholly owned, fully licensed captive insurance company for excess coverage. The state assessments are typically based on payroll amounts and, to a limited extent, the amount of permanent disability awards during the previous year. Excess insurance premiums are also based in part on the size and risk profile of our payroll and loss experience.

Workers Compensation Claims Experience and Reserves

We recognize our liability for the ultimate payment of incurred claims and claims adjustment expenses by accruing liabilities which represent estimates of future amounts necessary to pay claims and related expenses with respect to covered events that have occurred. When a claim involving a probable loss is reported, our internal claims management personnel or our TPA establishes a case reserve for the estimated amount of ultimate loss. The estimate reflects an informed judgment based on established case reserving practices and the experience and knowledge of our claims management staff and the TPA regarding the nature and expected value of the claim, as well as the estimated expense of settling the claim, including legal and other fees and expenses of administering claims. The adequacy of such case reserves in part depends on the professional judgment of both our claims management staff and our TPA to properly and comprehensively evaluate the economic consequences of each claim. Our reserves include an additional component for both estimated future adverse loss development in excess of initial case reserves on open claims and for incurred but not reported claims (together IBNR) based upon an actuarial estimate provided by the Companys independent actuary. Our reserves do not include an estimated provision for the incidence of unknown or unreported catastrophic claims.

As part of the case reserving process, historical data is reviewed and consideration is given to the anticipated effect of various factors, including known and anticipated legal developments, inflation and economic conditions. Reserve amounts are based on managements estimates, and as other data becomes available, these estimates are revised, which may result in increases or decreases in existing case reserves. Managements internal accrual process for workers compensation expense is based upon the immediate recognition of an expense and the related liability at the time a claim occurs; the value ascribed to the expense and liability is based upon our internal claims management and the TPAs estimate of ultimate claim cost coupled with a provision for estimated future development based upon an actuarial review performed quarterly by our independent actuary. We believe our total accrued workers compensation claims liabilities at December 31, 2012, are adequate. It is possible, however, that our actual future workers compensation obligations may exceed the amount of our accrued liabilities, with a corresponding negative effect on future earnings, due to such factors as unanticipated adverse loss development of known claims and, to a much lesser extent, of claims incurred but not reported.

Failure to successfully manage the severity and frequency of workplace injuries would result in increased workers compensation expense and would have a negative effect, which may be substantial, on our operating results and financial condition. Management maintains clear guidelines for our branch office managers, account managers, and risk managers directly tying their continued employment to their diligence in understanding and

addressing the risks of accident or injury associated with the industries in which client

- 10 -

Table of Contents

companies operate and in monitoring clients compliance with workplace safety requirements. We have a policy of zero tolerance for avoidable workplace injuries. Each of our risk managers has the authority to cancel any client at any time based upon their assessment of their safe-work practices or philosophies.

Employees and Employee Benefits

At December 31, 2012, we had approximately 64,315 employees, including approximately 7,700 staffing services employees, approximately 56,210 employees under our co-employment agreements, 405 managerial, sales and administrative employees and three executive officers. The number of employees at any given time may vary significantly due to business conditions at customer or client companies. During 2012, approximately 2% of our employees were covered by a collective bargaining agreement. Substantially all of our managerial, sales and administrative employees have entered into a standard form of employment agreement which, among other provisions, contains covenants not to engage in certain activities in competition with us for 18 months following termination of employment and to maintain the confidentiality of certain proprietary information. We believe our employee relations are good.

Benefits offered to our staffing services employees include a limited-benefit medical insurance plan, a Section 125 cafeteria plan which permits employees to use pretax earnings to fund various services, including health insurance premiums and childcare expenses, and a retirement savings plan (the 401(k) plan) under Section 401(k) of the Internal Revenue Code pursuant to which employees may begin making contributions upon reaching 21 years of age and completing 1,000 hours of service in any consecutive 12-month period. We may also make contributions to the 401(k) plan, which vest over six years and are subject to certain legal limits, at the sole discretion of our Board of Directors. We make matching contributions to the 401(k) plan under a safe harbor provision, whereby we match 100% of contributions by management and staffing employees to the 401(k) plan up to 3% of each participating employees annual compensation and 50% of the employees contributions up to an additional 2% of annual compensation. Employees subject to a co-employer arrangement may participate in our benefit plans at the election of the co-employer.

Regulatory and Legislative Issues

Business Operations. We are subject to the laws and regulations of the jurisdictions within which we operate, including those governing self-insured employers under the workers compensation systems in Oregon, California, Maryland, Delaware and Colorado, as well as in Washington for staffing and management employees. We are also subject to laws and regulations governing our two wholly owned, fully licensed insurance companies in Arizona. While the specific laws and regulations vary among these jurisdictions, they typically require some form of licensing and often have statutory requirements for workplace safety and notice of change in obligation of workers compensation coverage in the event of contract termination. Although compliance with these requirements imposes some additional financial risk on us, particularly with respect to those clients who breach their payment obligation to us, such compliance has not had a material adverse effect on our business to date.

Employee Benefit Plans. Our operations are affected by numerous federal and state laws relating to labor, tax and employment matters. Through our co-employment

- 11 -

Table of Contents

arrangement, we assume certain obligations and responsibilities as the administrative employer under federal and state laws. Because many of these federal and state laws were enacted prior to the development of nontraditional employment relationships, such as professional employer, temporary employment, and outsourcing arrangements, many of these laws do not specifically address the obligations and responsibilities of nontraditional employers. In addition, the definition of employer under these laws is not uniform.

As an employer, we are subject to all federal statutes and regulations governing our employer-employee relationships. Subject to the discussion of risk factors below, we believe that our operations are in compliance in all material respects with applicable federal statutes and regulations.

We offer various qualified employee benefit plans to our employees, including those employees for whom we are the administrative employer in a co-employment agreement who so elect. These qualified employee benefit plans include our 401(k) plan, a cafeteria plan under Section 125 of the Internal Revenue Code, and group health, life insurance and disability insurance plans. Generally, qualified employee benefit plans are subject to provisions of both the Internal Revenue Code and the Employee Retirement Income Security Act of 1974 (ERISA). In order to qualify for favorable tax treatment under the Internal Revenue Code, qualified plans must be established and maintained by an employer for the exclusive benefit of its employees.

Recent Legislative Developments in California Affecting Workers Compensation System

During September 2012, California Senate Bill 863 (SB 863), designed to reform Californias workers compensation system, was signed into law. Section 3701.9 of Section 16 of SB 863 was added to the Labor Code and includes a provision whereby the California Director of Self-Insurance is required not to issue certificates of consent to self-insure after January 1, 2013 to any employer engaged in the activities of a professional employer organization, a leasing employer, a temporary services employer or any employer the Director determines to be in the business of providing employees to other employers. Additionally, a certificate of consent to self-insure that previously had been issued to any employer engaged in these types of activities is required to be revoked by the Director not later than January 1, 2015. If the Company, which has a certificate of consent to self-insure in place, is not able to secure alternatives to address the impact of SB 863 on the Companys ability to continue its self-insurance program in California, our results of operations may be adversely affected. We are currently exploring several potential alternatives to address the impact of SB 863 on our ability to continue our self-insurance program in California. See Liquidity and Capital Resources in Item 7.

Additional Information

Our filings with the SEC, including our annual report on Form 10-K, quarterly reports on Form 10-Q, periodic reports on Form 8-K and amendments to these reports, are accessible free of charge at our website at http://www.barrettbusiness.com as soon as reasonably practicable after filing with the SEC. By making this reference to our website, we do not intend to incorporate into this report any information contained in the website. The website should not be considered part of this report.

- 12 -

Table of Contents

The SEC maintains a website at http://www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers with publicly traded securities, including the Company.

| Item 1A. | RISK FACTORS |

In addition to other information contained in this report, the following risk factors should be considered carefully in evaluating our business.

Our workers compensation loss reserves may be inadequate to cover our ultimate liability for workers compensation costs.

We maintain reserves (recorded as accrued liabilities on our balance sheet) to cover our estimated liabilities for our self-insured workers compensation claims. The determination of these reserves is based upon a number of factors, including current and historical claims activity, claims payment patterns and medical cost trends and developments in existing claims. Accordingly, reserves do not represent an exact calculation of liability. Reserves can be affected by both internal and external events, such as adverse developments on existing claims or changes in medical costs, medical condition of the claimant, claims handling procedures, administrative costs and legal fees, inflation, and legal trends and legislative changes. Reserves are adjusted from time to time to reflect new claims, claim developments, or systemic changes, and such adjustments are reflected in the results of the periods in which the reserves are changed. The Companys estimated accrual for workers compensation claims liabilities is based upon an actuarial estimate provided by the Companys independent actuary. The estimated accrual does not include an estimated provision for the incidence of unknown catastrophic claims. Moreover, because of the uncertainties that surround estimating workers compensation loss reserves, we cannot be certain that our reserves are adequate. If our reserves are insufficient to cover our actual losses, we would have to increase our reserves and incur charges to our earnings that could be material to our results of operations and financial condition.

Our self-insured retention for workers compensation claims is $5.0 million per occurrence in the majority of our self-insured states.

In view of the Companys favorable historical experience with large catastrophic claims and an opportunity to realize savings from lower excess workers compensation insurance premiums, we maintain our self-insured retention at $5.0 million per occurrence, except in Maryland and Colorado where our retention is at $1.0 million and $500,000 per occurrence, respectively. Additionally, Ecoles retention is at $5.0 million per occurrence for coverage in Arizona. Thus, the Company has financial risk for most workers compensation claims under $5.0 million, on a per occurrence basis. This level of per occurrence retention may result in higher workers compensation costs to us with a corresponding negative effect on our operating results and financial condition.

Adverse developments in the market for excess workers compensation insurance could lead to increases in our costs.

We are a state-approved self-insured employer for workers compensation coverage in California, Oregon, Delaware, Maryland and Colorado, as well as in Washington for our staffing

- 13 -

Table of Contents

and management employees. To manage our financial exposure in the event of catastrophic injuries or fatalities, we maintain excess workers compensation insurance with a per occurrence retention of $5.0 million effective January 1, 2007, except in Maryland and Colorado where our retention is at $1.0 million and $500,000 per occurrence, respectively. Additionally, Ecoles retention is at $5.0 million per occurrence for coverage in Arizona. Changes in the market for excess workers compensation insurance may lead to limited availability of such coverage, additional increases in our insurance costs or further increases in our self-insured retention, any of which may have a material adverse effect on our financial condition.

Economic conditions, particularly in California, may impact our ability to attract new clients and cause our existing PEO clients to reduce staffing levels or cease operations.

Weak economic conditions typically have a negative impact on small and medium size businesses, which make up the majority of our clients in a co-employment agreement. In turn, these businesses could cut costs, including trimming employees from their payrolls, or ceasing operations altogether. In addition, businesses may be reluctant to enter into new client service agreements because of the uncertainty regarding the timing of any economic recovery. These forces may result in decreased revenues due both to the downsizing of our current clients and difficulties in attracting new clients, and may also result in additional bad debt expense to the extent that existing clients cease operations.

Our staffing business is vulnerable to economic fluctuations. Companies tend to use fewer temporary employees as economic activity slows and recruiting employees to fill our customers needs becomes increasingly difficult during robust economic periods.

Demand for our staffing services is sensitive to changes in the level of economic activity in the regions in which we do business. As economic activity slows down, companies often reduce their use of temporary employees before undertaking layoffs of permanent staff, resulting in decreased demand for staffing services. During strong economic periods, on the other hand, we often experience shortages of qualified employees to meet customer needs.

Changes in the market for workers compensation insurance in the state of California could adversely affect our business.

Our concentration of business in California subjects our business to market risks involving the California workers compensation environment as the Company is a state-approved self-insured employer with respect to workers compensation coverage in that state. During recent years, California has enacted several legislative reforms in an attempt to address the crisis in its workers compensation system, and it may attempt additional legislative or regulatory reforms in the future. Any successful legislative reforms or non-governmental changes in market conditions in California could lessen a key advantage we have in that state, leading to a reduction in our new business opportunities and a potential slowing in the growth of our business in California. Any such slowing would adversely affect our results of operations.

During September 2012, California Senate Bill 863 (SB 863), designed to reform Californias workers compensation system, was signed into law. Section 3701.9 of Section 16 of SB 863 was added to the Labor Code and includes a provision whereby the California

- 14 -

Table of Contents

Director of Self-Insurance is required not to issue certificates of consent to self-insure after January 1, 2013 to any employer engaged in the activities of a professional employer organization, a leasing employer, a temporary services employer or any employer the Director determines to be in the business of providing employees to other employers. Additionally, a certificate of consent to self-insure that previously had been issued to any employer engaged in these types of activities is required to be revoked by the Director not later than January 1, 2015. If the Company, which has a certificate of consent to self-insure in place, is not able to secure alternatives to address the impact of SB 863 on the Companys ability to continue its self-insurance program in California, our results of operations may be adversely affected.

Because we assume the obligation to make wage, tax and regulatory payments in respect of some employees, we are exposed to client credit risks.

We generally assume responsibility for and manage the risks associated with our clients employee payroll obligations, including liability for payment of salaries and wages (including payroll taxes), as well as group health and retirement benefits. These obligations are fixed, whether or not the client makes payments to us as required by our services agreement, which exposes us to credit risks. We attempt to mitigate this risk by invoicing our staffing customers weekly and our clients in co-employment agreements at the end of their specific payroll processing cycle. We also carefully monitor the timeliness of our clients payments and impose strict credit standards on our customers. If we fail to successfully manage our credit risk, our results of operations and financial condition could be materially and adversely affected.

Increases in unemployment claims could raise our state and federal unemployment tax rates which we may not be able to pass on to our customers.

During weak economic conditions in our markets, the level of unemployment claims tend to rise as a result of employee layoffs at our clients and lack of work in our temporary staffing pool. The rise in unemployment claims often results in higher state and federal unemployment tax rates which in most instances cannot be concurrently passed on to our customers either due to existing client services agreements or competitive pricing pressures. Increases in our state and federal unemployment tax rates could have a material adverse effect on our results of operations, particularly in the early part of the calendar year when effective payroll tax rates are at or near their maximum.

If we are determined not to be an employer under certain laws and regulations, our clients may stop using our services, and we may be subject to additional liabilities.

We are the administrative employer in our co-employment relationships under the various laws and regulations of the Internal Revenue Service and the U.S. Department of Labor. If we are determined not to be the administrative employer under such laws and regulations and are therefore unable to assume our clients obligations for employment and other taxes, our clients may be held jointly and severally liable for payment of such taxes. Some clients or prospective clients may view such potential liability as an unacceptable risk, discouraging current clients from continuing a relationship with us or prospective clients from entering into a new relationship with us. Any determination that we are not the administrative employer for purposes of ERISA could adversely affect our cafeteria benefits plan operated under Section 125 of the Internal Revenue Code and result in liabilities to us under the plan.

- 15 -

Table of Contents

We may be exposed to employment-related claims and costs and periodic litigation that could adversely affect our business and results of operations.

We either co-employ employees in connection with our client services agreements or place our employees in our customers workplace in connection with our staffing business. As such, we are subject to a number of risks inherent to our status as the administrative employer, including without limitation:

| | claims of misconduct or negligence on the part of our employees, discrimination or harassment claims against our employees, or claims by our employees of discrimination or harassment by our clients; |

| | immigration-related claims; |

| | claims relating to violations of wage, hour and other workplace regulations; |

| | claims relating to employee benefits, entitlements to employee benefits, or errors in the calculation or administration of such benefits; and |

| | possible claims relating to misuse of customer confidential information, misappropriation of assets or other similar claims. |

If we experience significant incidents involving any of the above-described risk areas we could face substantial out-of-pocket losses, fines or negative publicity. In addition, such claims may give rise to litigation, which may be time consuming, distracting and costly, and could have a material adverse effect on our business. With respect to claims involving our co-employer relationships, although our client services agreement provides that the client will indemnify us for any liability attributable to the conduct of the client or its employees, we may not be able to enforce such contractual indemnification, or the client may not have sufficient assets to satisfy its obligations to us.

We operate in a complex regulatory environment, and failure to comply with applicable laws and regulations could adversely affect our business.

Corporate human resource operations are subject to a broad range of complex and evolving laws and regulations, including those applicable to payroll practices, benefits administration, employment practices and privacy. Because our clients have employees in many states throughout the United States, we must perform our services in compliance with the legal and regulatory requirements of multiple jurisdictions. Some of these laws and regulations may be difficult to ascertain or interpret and may change from time to time. Violation of such laws and regulations could subject us to fines and penalties, damage our reputation, constitute a breach of our client agreements, impair our ability to obtain and renew required licenses, and decrease our profitability or competitiveness. If any of these effects were to occur, our operating results and financial condition could be adversely affected.

- 16 -

Table of Contents

Changes in government regulations may result in restrictions or prohibitions applicable to the provision of employment services or the imposition of additional licensing, regulatory or tax requirements.

Our business is heavily regulated in most jurisdictions in which we operate. We cannot assure you that the states in which we conduct or seek to conduct business will not:

| | impose additional regulations that prohibit or restrict employment-related businesses like ours; |

| | require additional licensing or add restrictions on existing licenses to provide employment-related services; or |

| | increase taxes or make changes in the way in which taxes are calculated for providers of employment-related services. |

Any changes in applicable laws and regulations may make it more difficult or expensive for us to do business, inhibit expansion of our business, or result in additional expenses that limit our profitability or decrease our ability to attract and retain clients.

The tax status of our insurance subsidiaries could be challenged resulting in an acceleration of income tax payments.

In conjunction with our workers compensation program, we operate two wholly owned insurance subsidiaries, AICE and Ecole. We recognize the two subsidiaries as insurance companies for federal income tax purposes, with respect to our consolidated federal income tax return. In the event the Internal Revenue Service (IRS) were to determine that the subsidiaries do not qualify as insurance companies, we could be required to make accelerated income tax payments to the IRS that we otherwise would have deferred until future periods.

We may find it difficult to expand our business into additional states due to varying state regulatory requirements.

Future growth in our operations depends, in part, on our ability to offer our services to prospective clients in new states, which may subject us to different regulatory requirements and standards. In order to operate effectively in a new state, we must obtain all necessary regulatory approvals, adapt our procedures to that states regulatory requirements and modify our service offerings to adapt to local market conditions. In the event that we expand into additional states, we may not be able to duplicate in other markets the financial performance experienced in our current markets.

Acquisitions subject us to various risks, including risks relating to selection and pricing of acquisition targets, integration of acquired companies into our business and assumption of unanticipated liabilities.

We have completed 27 acquisitions since 1993 and may pursue additional acquisitions and investment opportunities. We cannot assure, however, that we will be able to identify or complete additional acquisitions. If we do pursue acquisitions, we may not realize the

- 17 -

Table of Contents

anticipated benefits of such acquisitions. Acquisitions involve many risks, including risks relating to the assumption of unforeseen liabilities of an acquired business, adverse accounting charges resulting from the acquisition, and difficulties in integrating acquired companies into our business, both from a cultural perspective, as well as with respect to personnel and client retention and technological integration. Acquired liabilities may be significant and may adversely affect our financial condition and results of operations. Our inability to successfully integrate acquired businesses may lead to increased costs, failure to generate expected returns, accounting charges, or even a total loss of amounts invested, any of which could have a material adverse effect on our financial condition and results of operations.

Our business is subject to risks associated with geographic market concentration.

Our California and Oregon operations accounted for approximately 69% and 10%, respectively, of our total net revenues in 2012. As a result of the current importance of our California and Oregon operations and anticipated continued growth from these operations, our profitability over the next several years is expected to be largely dependent on economic and regulatory conditions in these markets, particularly in California. If these states experience a further economic downturn, or if the regulatory environment changes in a way that adversely affects our ability to do business in these states or limits our competitive advantages in these markets, our profitability and growth prospects may be materially and adversely affected.

We face competition from a number of other companies.

We face competition from various companies that may provide all or some of the services we offer. Our competitors include companies that are engaged in staffing services such as Kelly Services, Inc. and Manpower Inc., companies that are focused on co-employment, such as Insperity, Inc. and companies that primarily provide payroll processing services, such as Automatic Data Processing, Inc. and Paychex, Inc. We also face competition from information technology outsourcing firms and broad-based outsourcing and consulting firms that perform individual projects.

Several of our existing or potential competitors have substantially greater financial, technical and marketing resources than we do, which may enable them to:

| | develop and expand their infrastructure and service offerings more quickly and achieve greater cost efficiencies; |

| | invest in new technologies; |

| | expand operations into new markets more rapidly; |

| | devote greater resources to marketing; |

| | compete for acquisitions more effectively and complete acquisitions more easily; and |

| | aggressively price products and services and increase benefits in ways that we may not be able to match financially. |

In order to compete effectively in our markets, we must target our potential clients carefully, continue to improve our efficiencies and the scope and quality of our services, and

- 18 -

Table of Contents

rely on our service quality, innovation, education and program clarity. If our competitive advantages are not compelling or sustainable, then we are unlikely to increase or sustain profits and our stock price could decline.

We are dependent upon certain key personnel and recruitment and retention of key employees may be difficult and expensive.

We believe that the successful operation of our business is dependent upon our retention of the services of key personnel, including our Chief Executive Officer, other executive officers and branch managers. We may not be able to retain all of our executives, senior managers and key personnel in light of competition for their services. If we lose the services of one of our executive officers or a significant number of our senior managers, our operations and profitability likely would be adversely affected.

We do not have an expansive in-house sales staff and therefore rely extensively on referral partners

We maintain only a minimal internal professional sales force. Instead, we rely heavily on referral partners to provide referrals to new business, especially in California, although each area manager is expected to be an effective leader in business development, including marketing efforts and sales closures. In connection with these arrangements, we pay a fee to referral partners for new clients. As a result, we are dependent on firms and individuals that do not have an exclusive relationship with us. If we are unable to maintain these relationships, if they increase their fees or lose confidence in our services, we could face declines in our business and additional costs and uncertainties as we attempt to hire and train an internal sales force.

We depend on attracting and retaining qualified employees; during periods of economic growth, our costs to do so increase and it becomes more difficult to attract and retain people.

The success of our staffing services depends on our ability to attract and retain qualified employees for placement with our customers. Our ability to attract and retain qualified personnel could be impaired by rapid improvement in economic conditions resulting in lower unemployment and increases in compensation. During periods of economic growth, we face growing competition for retaining and recruiting qualified personnel, which in turn leads to greater advertising and recruiting costs and increased salary expenses. If we cannot attract and retain qualified employees, the quality of our services may deteriorate and our reputation and results of operations could be adversely affected.

Our service agreements may be terminated on short notice, leaving us vulnerable to loss of a significant amount of customers in a short period of time, if business or regulatory conditions change or events occur that negatively affect our reputation.

Our client services agreements are generally terminable on 30 days notice by either us or the client. As a result, our clients may terminate their agreement with us at any time, making us particularly vulnerable to changing business or regulatory conditions or changes affecting our reputation or the reputation of our industry.

- 19 -

Table of Contents

Our industry has at times received negative publicity that, if it were to become more prevalent, could cause our business to decline.

In the industries in which we compete, companies periodically have been tarnished by negative publicity or scandals from poor business judgment or even outright fraud. If we or our industry face negative publicity, customers confidence in the use of temporary personnel or co-employed workers may deteriorate, and they may be unwilling to enter into or continue our staffing or co-employment relationships. If a negative perception were to prevail, it would be more difficult for us to attract and retain customers.

Changes in state unemployment tax laws and regulations could adversely affect our business.

In past years, there has been significant negative publicity relating to the use of staffing or PEO companies to shield employers from poor unemployment history and high unemployment taxes. New legislation enacted at the state or federal level to try to counter this perceived problem could have a material adverse effect on our business by limiting our ability to market our services or making our services less attractive to our customers and potential customers.

We are dependent upon technology services and if we experience damage, service interruptions or failures in our computer and telecommunications systems, or if our security measures are breached, our client relationships and our ability to attract new clients may be adversely affected.

Our business could be interrupted by damage to or disruption of our computer and telecommunications equipment and software systems, and we may lose data. Our clients businesses may be adversely affected by any system or equipment failure we experience. As a result of any of the foregoing, our relationships with our clients may be impaired, we may lose clients, our ability to attract new clients may be adversely affected and we could be exposed to contractual liability. Precautions in place to protect ourselves from, or minimize the effect of, such events, may not be adequate.

In addition, our business involves the storage and transmission of clients proprietary information and confidential personal data of employees. Security breaches could expose us to a risk of loss of this information, litigation and possible liability. If our security measures are breached as a result of third-party action, employee error, malfeasance or otherwise, and, as a result, someone obtains unauthorized access to client or employee data, our reputation will be damaged, our business may suffer and we could incur significant liability. Techniques used to obtain unauthorized access or to sabotage systems change frequently and are growing increasingly sophisticated. As a result, we may be unable to anticipate these techniques or to implement adequate preventative measures. If an actual or perceived breach of our security occurs, we could be liable and the market perception of our services could be harmed.

- 20 -

Table of Contents

Maryland law and our Charter and bylaws contain provisions that could make the takeover of the Company more difficult.

Certain provisions of Maryland law and our Charter and bylaws could have the effect of delaying or preventing a third party from acquiring the Company, even if a change in control would be beneficial to our stockholders. These provisions of our Charter and bylaws:

| | permit the Board of Directors to issue up to 500,000 shares of preferred stock with such rights and preferences, including voting rights, as the Board may establish, without further approval by the Companys stockholders, which could also adversely affect the voting power of holders of our common stock; and |

| | vest the power to adopt, alter or repeal the Companys bylaws solely in the Board of Directors; the stockholders do not have that power. |

In addition, the Company is subject to the Maryland control share act (the Control Share Act). Under the Control Share Act, a person (an Acquiring Person) who acquires voting stock in a transaction (a Control Share Acquisition) which results in its holding voting power within specified ranges cannot vote the shares it acquires in the Control Share Acquisition unless voting rights are accorded to such control shares by the holders of two-thirds of the outstanding voting shares, excluding the Acquiring Person and the Companys officers and directors who are also employees of the Company.

The Company is also subject to the provisions of Maryland law limiting the ability of certain Maryland corporations to engage in specified business combinations (the Business Combination Act). Subject to certain exceptions, the Business Combination Act prohibits a Maryland corporation from engaging in a business combination with a stockholder who, with its affiliates, owns 10% or more of the corporations voting stock. These provisions will not apply to business combinations that are approved by the Board of Directors before the stockholder became an interested stockholder.

| Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

- 21 -

Table of Contents

| Item 2. | PROPERTIES |

We operate through all 50 of our branch offices. The following table shows the number of locations in each state in which we operate. We also lease office space in other locations in our market areas which we use to recruit and place employees.

| Offices |

Number of Locations |

|||

| California |

18 | |||

| Oregon |

11 | |||

| Utah |

5 | |||

| Washington |

5 | |||

| Idaho |

3 | |||

| Arizona |

2 | |||

| Colorado |

2 | |||

| Maryland |

2 | |||

| Delaware |

1 | |||

| North Carolina |

1 | |||

We lease office space for our branch offices. At December 31, 2012, our leases had expiration dates ranging from less than one year to five years, with total minimum payments through 2017 of approximately $8.5 million. Our corporate headquarters office in Vancouver, Washington occupies approximately 32 percent of the 63,500 square foot building we own.

| Item 3. | LEGAL PROCEEDINGS |

See Note 14, Litigation, in the Notes to Consolidated Financial Statements included in Item 15 of this report.

| Item 4. | MINE SAFETY DISCLOSURES |

Not Applicable

EXECUTIVE OFFICERS OF THE REGISTRANT

The following table identifies, as of March 15, 2013, each executive officer of the Company. Executive officers are elected annually and serve at the discretion of the Board of Directors.

| Name |

Age | Principal Positions and Business Experience |

Officer Since |

|||||||

| Michael L. Elich |

47 | President and Chief Executive Officer | 2005 | |||||||

| James D. Miller |

49 | Vice President-Finance, Treasurer and Secretary; Chief Financial Officer; Principal Accounting Officer | 1994 | |||||||

| Gregory R. Vaughn |

57 | Vice President and Assistant Secretary; Chief Administrative Officer |

1998 | |||||||

Michael L. Elich joined the Company in October 2001 as Director of Business Development. He was appointed Vice President and Chief Operating Officer in May 2005. He

- 22 -

Table of Contents

was appointed interim President and Chief Executive Officer in January 2011 upon the death of William W. Sherertz. Effective February 17, 2011, Mr. Elich was elected to serve on the Board of Directors and was made President and Chief Executive Officer. From 1995 to 2001, Mr. Elich served as Executive Vice President and Chief Operating Officer of Skills Resource Training Center, a staffing services company with offices in Oregon, Washington and Idaho that we acquired in 2004.

James D. Miller joined the Company in January 1994 as Controller. He was promoted to Vice President-Finance, Treasurer and Secretary, and Chief Financial Officer in June 2008. From 1991 to 1994, he was the Corporate Accounting Manager for Christensen Motor Yacht Corporation. Mr. Miller, a certified public accountant on inactive status, was employed by Price Waterhouse LLP, now known as PricewaterhouseCoopers LLP, from 1987 to 1991.

Gregory R. Vaughn joined the Company in July 1997 as Operations Manager. Mr. Vaughn was appointed Vice President in January 1998 and Chief Administrative Officer in February 2012. Prior to joining Barrett, Mr. Vaughn was Chief Executive Officer of Insource America, Inc., a privately-held human resource management company headquartered in Portland, Oregon, for approximately one year. Mr. Vaughn has also held senior management positions with Sundial Time Systems, Inc., and Continental Information Systems, Inc. Previously, Mr. Vaughn was employed as a technology consultant by Price Waterhouse LLP, now known as PricewaterhouseCoopers LLP.

- 23 -

Table of Contents

| Item 5. | MARKET FOR REGISTRANTS COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common stock (the Common Stock) trades on the Global Select Market segment of The Nasdaq Stock Market under the symbol BBSI. At March 1, 2013, there were 28 stockholders of record and approximately 1,560 beneficial owners of the Common Stock.

The following table presents the high and low sales prices of the Common Stock and cash dividends paid for each quarterly period during the last two fiscal years, as reported by The Nasdaq Stock Market. Any future determination as to the payment of dividends will be made at the discretion of the Board and will depend upon the Companys operating results, financial condition, capital requirements, general business conditions and such other factors as the Board deems relevant.

| High | Low | Cash Dividends Declared |

||||||||||

| 2011 |

||||||||||||

| First Quarter |

$ | 16.22 | $ | 13.50 | $ | 0.09 | ||||||

| Second Quarter |

16.83 | 13.76 | 0.09 | |||||||||

| Third Quarter |

15.77 | 12.25 | 0.09 | |||||||||

| Fourth Quarter |

20.00 | 13.49 | 0.11 | |||||||||

| 2012 |

||||||||||||

| First Quarter |

$ | 21.10 | $ | 15.68 | $ | 0.11 | ||||||

| Second Quarter |

21.45 | 18.88 | 0.11 | |||||||||

| Third Quarter |

28.96 | 19.99 | 0.11 | |||||||||

| Fourth Quarter |

39.49 | 26.19 | 0.13 | |||||||||

The Company maintains a Board approved stock repurchase program which currently authorizes shares to be repurchased up to 3.0 million shares of the Companys stock from time to time in open market purchases. The following table summarizes information related to stock repurchases during the quarter ended December 31, 2012.

| Month |

Shares Repurchased |

Average Price Per Share |

Total Number of Shares Repurchased as Part of Publicly Announced Plan |

Maximum Number of Shares that May Yet Be Repurchased Under the Plan |

||||||||||||

| October |

0 | 0 | 0 | 1,208,200 | ||||||||||||

| November |

0 | 0 | 0 | 1,208,200 | ||||||||||||

| December |

0 | 0 | 0 | 1,208,200 | ||||||||||||

|

|

|

|

|

|||||||||||||

| Total |

0 | 0 | ||||||||||||||

|

|

|

|

|

|||||||||||||

- 24 -

Table of Contents

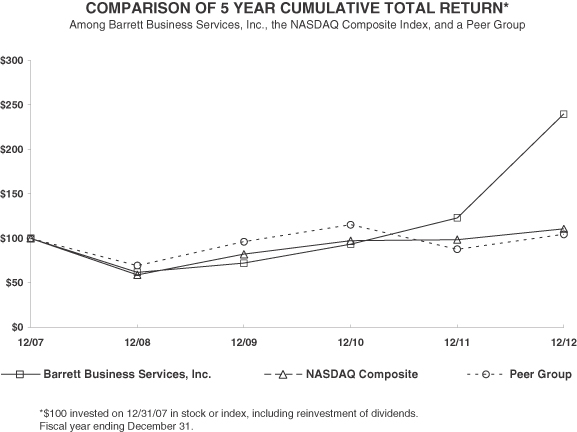

The following graph shows the cumulative total return at the dates indicated for the period from December 31, 2007, until December 31, 2012, for our Common Stock, The Nasdaq Composite Index, and a group of the Companys current peers in the staffing industry (the 2012 Peer Group). The 2012 Peer Group is comprised of five companies included in the peer group used to prepare the performance graph included in the Companys Form 10-K for the year ended December 31, 2011.

The stock performance graph has been prepared assuming that $100 was invested on December 31, 2007, in our Common Stock, The Nasdaq Composite Index, and the 2012 Peer Group, and that dividends are reinvested. In accordance with the SECs disclosure rules, the stockholder return for each company in the 2012 Peer Group indices has been weighted on the basis of market capitalization as of the beginning of each annual period shown. The stock price performance reflected in the graph may not be indicative of future price performance.

| 12/07 | 12/08 | 12/09 | 12/10 | 12/11 | 12/12 | |||||||||||||||||||

| Barrett Business Services, Inc. |

100.00 | 62.01 | 72.17 | 93.58 | 123.11 | 239.78 | ||||||||||||||||||

| NASDAQ Composite |

100.00 | 59.03 | 82.25 | 97.32 | 98.63 | 110.78 | ||||||||||||||||||

| Peer Group |

100.00 | 69.52 | 96.26 | 115.37 | 87.84 | 104.58 | ||||||||||||||||||

| Members of Peer Group |

||||||||||||||||||||||||

| CDI Corp. |

||||||||||||||||||||||||

| Insperity Inc |

||||||||||||||||||||||||

| Kelly Services Inc |

||||||||||||||||||||||||

| Manpowergroup |

||||||||||||||||||||||||

| Robert Half International Inc |

||||||||||||||||||||||||

- 25 -

Table of Contents

| Item 6. | SELECTED CONSOLIDATED FINANCIAL DATA |

The following selected consolidated financial data should be read in conjunction with the Companys financial statements and the accompanying notes listed in Item 8 of Part II, Financial Statements and Supplementary Data, and the information contained in Item 7 of Part II, Managements Discussion and Analysis of Financial Condition and Results of Operations. Historical results are not necessarily indicative of future results.

| Year Ended December 31, | ||||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

| (In thousands, except per share data) | ||||||||||||||||||||

| Statement of operations: |

||||||||||||||||||||

| Revenues: |

||||||||||||||||||||

| Professional employer service fees |

$ | 276,004 | $ | 190,113 | $ | 147,385 | $ | 120,305 | $ | 125,903 | ||||||||||

| Staffing services |

126,648 | 124,761 | 125,738 | 116,155 | 154,565 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

402,652 | 314,874 | 273,123 | 236,460 | 280,468 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Cost of revenues: |

||||||||||||||||||||

| Direct payroll costs |

95,128 | 94,568 | 95,439 | 87,679 | 114,440 | |||||||||||||||

| Payroll taxes and benefits |

169,724 | 123,017 | 96,660 | 82,077 | 85,531 | |||||||||||||||

| Workers' compensation |

71,086 | 53,837 | 36,284 | 39,765 | 31,166 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

335,938 | 271,422 | 228,383 | 209,521 | 231,137 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross margin |

66,714 | 43,452 | 44,740 | 26,939 | 49,331 | |||||||||||||||

| Selling, general and administrative expenses |

46,450 | 38,174 | 35,429 | 33,481 | 36,654 | |||||||||||||||

| Depreciation and amortization |

1,477 | 1,344 | 1,395 | 1,641 | 1,536 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from operations |

18,787 | 3,934 | 7,916 | (8,183 | ) | 11,141 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Other income (loss): |

||||||||||||||||||||

| Life insurance proceeds |