10-K: Annual report pursuant to Section 13 and 15(d)

Published on March 3, 2020

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

Commission File Number 0-21886

BARRETT BUSINESS SERVICES, INC.

(Exact name of registrant as specified in its charter)

|

Maryland |

|

52-0812977 |

|

(State or other jurisdiction of |

|

(IRS Employer |

|

incorporation or organization) |

|

Identification No.) |

|

|

|

|

|

8100 NE Parkway Drive, Suite 200 |

|

|

|

Vancouver, Washington |

|

98662 |

|

(Address of principal executive offices) |

|

(Zip Code) |

(360) 828-0700

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

|

Common Stock, Par Value $0.01 Per Share |

BBSI |

The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐ |

Accelerated filer ☒ |

Non-accelerated filer ☐ |

Smaller reporting company ☐ |

|

Emerging growth company ☐ |

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

State the aggregate market value of the common equity held by non-affiliates of the registrant: $585,585,998 at June 30, 2019

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date:

|

Class |

Outstanding at February 18, 2020 |

|

Common Stock, Par Value $.01 Per Share |

7,528,576 Shares |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for the 2020 Annual Meeting of Stockholders are hereby incorporated by reference in Part III of Form 10-K.

BARRETT BUSINESS SERVICES, INC.

2019 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

|

|

|

|

Page |

|

|

Item 1. |

|

|

2 |

|

|

|

|

|

|

|

|

Item 1A. |

|

|

9 |

|

|

|

|

|

|

|

|

Item 1B. |

|

|

18 |

|

|

|

|

|

|

|

|

Item 2. |

|

|

19 |

|

|

|

|

|

|

|

|

Item 3. |

|

|

19 |

|

|

|

|

|

|

|

|

Item 4. |

|

|

19 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 5. |

|

|

19 |

|

|

|

|

|

|

|

|

Item 6. |

|

|

21 |

|

|

|

|

|

|

|

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

22 |

|

|

|

|

|

|

|

Item 7A. |

|

|

31 |

|

|

|

|

|

|

|

|

Item 8. |

|

|

32 |

|

|

|

|

|

|

|

|

Item 9. |

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

|

59 |

|

|

|

|

|

|

|

Item 9A. |

|

|

59 |

|

|

|

|

|

|

|

|

Item 9B. |

|

|

62 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 10. |

|

|

62 |

|

|

|

|

|

|

|

|

Item 11. |

|

|

62 |

|

|

|

|

|

|

|

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

62 |

|

|

|

|

|

|

|

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

62 |

|

|

|

|

|

|

|

Item 14. |

|

|

62 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 15. |

|

|

63 |

|

|

|

|

|

|

|

|

Item 16. |

|

|

67 |

|

|

|

|

|

||

|

|

68 |

|||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

||

|

|

|

|

||

1

General

Company Background

Barrett Business Services, Inc. (“BBSI,” the “Company,” “our” or “we”), is a leading provider of business management solutions for small and mid-sized companies. The Company has developed a management platform that integrates a knowledge-based approach from the management consulting industry with tools from the human resource outsourcing industry. This platform, through the effective leveraging of human capital, helps our business owner clients run their businesses more effectively. We believe this platform, delivered through a decentralized organizational structure, differentiates BBSI from our competitors. BBSI was incorporated in Maryland in 1965.

Certain statements below contain forward-looking information that is subject to risks and uncertainties. See “Forward-Looking Information” in Item 7 of Part II of this report and “Risk Factors” in Item 1A of Part I of this report.

Business Strategy

Our strategy is to align local operations teams with the mission of small and mid-sized business owners, driving value to their business. To do so, BBSI:

|

|

• |

partners with business owners to leverage their investment in human capital through a high-touch, results-oriented approach; |

|

|

• |

brings predictability to each client organization through a three-tiered management platform; and |

|

|

• |

enables business owners to focus on their core business by reducing organizational complexity and maximizing productivity. |

Business Organization

We operate a decentralized delivery model using operationally-focused business teams, typically located within 50 miles of our client companies. These teams are led by senior level business generalists and comprise senior level professionals with expertise in human resources, organizational development, risk mitigation and workplace safety, and various types of administration, including payroll. These teams are responsible for growth of their operations, and for providing strategic leadership, guidance and expert consultation to our client companies. The decentralized structure fosters autonomous decision-making in which business teams deliver plans that closely align with the objectives of each business owner client. This structure also provides a means of incubating talent to support increased growth and capacity. We support clients with employees located in 29 states and the District of Columbia through a network of 64 branch locations in California, Oregon, Utah, Washington, Colorado, Idaho, Arizona, Maryland, North Carolina, Nevada, Pennsylvania, Delaware and Virginia. We also have several smaller recruiting locations in our general market areas, which are under the direction of a branch office.

BBSI believes that making significant investments in the best talent available allows us to leverage the value of this investment many times over. We motivate our management employees through a compensation package that includes a competitive base salary and the opportunity for profit sharing. At the branch level, profit sharing is in direct correlation to client performance, reinforcing a culture focused on achievement of client goals.

2

BBSI’s core purpose is to advocate for business owners, particularly in the small and mid-sized business segment. Our evolution from an entrepreneurially run company to a professionally managed organization has helped to form our view that all businesses experience inflection points at key stages of growth. The insights gained through our own growth, along with the trends we see in working with more than 7,200 companies each day, define our approach to guiding business owners through the challenges associated with being an employer. BBSI’s business teams align with each business owner client through a structured three-tiered progression. In doing so, business teams focus on the objectives of each business owner and deliver planning, guidance and resources in support of those objectives.

Tier 1: Tactical Alignment

The first stage focuses on the mutual setting of expectations and is essential to a successful client relationship. It begins with a process of assessment and discovery in which the business owner’s business objectives, attitudes, and culture are aligned with BBSI’s processes, controls and culture. This stage includes an implementation process, which addresses the administrative components of employment.

Tier 2: Dynamic Relationship

The second stage of the relationship emphasizes organizational development as a means of achieving each client’s business objectives. There is a focus on process improvement, development of best practices, supervisor training and leadership development.

Tier 3: Strategic Counsel

With an emphasis on advocacy on behalf of the business owner, the third stage of the relationship is more strategic and forward-looking with a goal of cultivating an environment in which all efforts are directed by the mission and long-term objectives of the business owner.

In addition to serving as a resource and guide, BBSI has the ability to provide workers’ compensation coverage as a means of meeting statutory requirements and protecting our clients from employment-related injury claims. Through our third-party administrators, we provide claims management services for our clients. We work aggressively to manage and reduce job injury claims, identify fraudulent claims and structure optimal work programs, including modified duty.

Categories of Services

We report financial results in two categories of services: Professional Employer Services (“PEO”) and Staffing. See Item 7 of this Report for information regarding the percentages of total net revenues provided by our PEO and staffing services for each of the last three fiscal years, and our consolidated financial statements in Item 8 of Part II of this Report for information regarding revenues, net income and total assets in our single reportable segment.

PEO

We enter into a client services agreement to establish a co-employment relationship with each client company, assuming responsibility for payroll, payroll taxes, workers’ compensation coverage (if elected) and certain other administrative functions for the client’s existing workforce. The client maintains physical care, custody and control of their workforce, including the authority to hire and terminate employees. During 2019, we supported in excess of 7,200 PEO clients with approximately 200,000 employees. This compares to more than 6,400 PEO clients and approximately 195,000 employees during 2018.

3

Our staffing services include on-demand or short-term staffing assignments, contract staffing, direct placement, and long-term or indefinite-term on-site management. On-site management employees are BBSI management employees who are based on the client-site and whose jobs are to assist BBSI staffing employees. Our recruiting experts maintain a deep network of professionals from which we source candidates. Through an assessment process, we gain an understanding of the short and long-term needs of our clients, allowing us to identify and source the right talent for each position. We then conduct a rigorous screening process to help ensure a successful hire.

Clients and Client Contracts

Our business is typically characterized by long-term relationships that result in recurring revenue. The terms and conditions applicable to our client relationships are set forth in a client services agreement, which typically provides for an initial term of one year with renewal for additional one-year periods, but generally permits cancellation by either party upon 30 days’ written notice. In addition, we may terminate the agreement at any time for specified breach of contract, including nonpayment or failure to follow our workplace safety recommendations.

The client services agreement also provides for indemnification by the client against losses arising out of any default by the client under the agreement, including failure to comply with any employment-related, health and safety, or immigration laws or regulations. Our client service agreement requires that clients enter into a co-employment arrangement and maintain comprehensive liability coverage in the amount of $1.0 million for acts of their employees. It is nevertheless possible that claims not satisfied through indemnification or insurance may be asserted against us, which could adversely affect our results of operations.

We have client services agreements with a diverse array of customers, including electronics manufacturers, various light-manufacturing industries, agriculture-based companies, transportation and shipping enterprises, food processors, telecommunications companies, public utilities, general contractors in various construction-related fields, and professional services firms. None of our clients individually represented more than 1% of our total revenues in 2019.

Market Opportunity

As a company that aligns with the mission of business owners by providing resources and guidance to small and mid-size businesses, BBSI believes its growth is driven by the desire of business owners to focus on mission-critical functions, reduce complexity associated with the employment function, mitigate costs and maximize their investment in human capital. Our integrated management platform has enabled us to capitalize on these needs within the small to mid-size business sector.

The small and mid‑sized business segment is particularly attractive because:

|

|

• |

it is large, continues to offer significant growth opportunity and remains underserved by professional services companies; |

|

|

• |

it typically has fewer in-house resources than larger businesses and, as a result, is generally more dependent on external resources; |

|

|

• |

we generally experience a relatively high client retention rate and lower client acquisition costs within this market segment; and |

|

|

• |

we have found that small to mid-sized businesses are responsive to quality of service when selecting a PEO or staffing services provider. |

4

The business environment in which we operate is characterized by intense competition and fragmentation. BBSI is not aware of reliable statistics regarding the number of its competitors, but certain large, well-known companies typically compete with us in the same markets and also have greater financial and marketing resources than we do, including Automatic Data Processing, Inc., ManpowerGroup, Inc., Kelly Services, Inc., Insperity, Inc., TriNet Group, Inc., Robert Half International Inc. and Paychex, Inc. We face additional competition from regional providers and we may in the future also face competition from new entrants to the field, including other staffing services companies, payroll processing companies and insurance companies. The principal competitive factors in the business environment in which we operate are price and level of service.

We believe that our growth is attributable to our ability to provide small and mid-sized companies with the resources and knowledge base of a large employer delivered through a local operations team. Our level of integration with each client business provides us an additional competitive advantage.

Growth Strategy

We believe our clients are our best advocates and powerful drivers of referral-based growth. In each market, operations teams provide expertise, consultation and support to our clients, driving growth and supporting retention. We anticipate that by adding business teams to existing branches, we can achieve incremental growth in those markets, driven by our reputation and by client referrals. While in most markets business development efforts are led by area managers, in some markets our sales efforts are further supported by business development managers.

Our business growth has three primary sources: referrals from existing clients, direct business-to-business sales efforts by our area managers, and an extensive referral network. Partners in our referral network include insurance brokers, financial advisors, attorneys, CPA’s, and other business professionals who can facilitate an introduction to prospective clients. These referral partners facilitate introductions to business owners on our behalf, typically in exchange for a fee equal to a small percentage of payroll.

We see two key drivers to our growth:

|

|

• |

Increase market share in existing markets. We seek to support, strengthen and expand branch office operations through the ongoing development of business teams. We believe that strengthening and expanding the operations of each location is an efficient and effective means of increasing market share in the geographic areas in which we do business, and that our business teams serve a dual purpose: 1) Delivering high-quality service to our clients, thereby supporting client business growth and retention, and driving client referrals, and 2) Incubating talent at the branch level to support expansion into new markets. |

|

|

• |

Penetrate new markets. We intend to open additional branch offices in new geographic markets as opportunities arise. We have developed a strategic approach to geographic expansion, which will serve as a guide for determining if and when to enter new markets. We believe our decentralized organizational model built on teams of senior-level professionals allows us to incubate talent to support our expansion efforts. |

5

Through our client services agreement, BBSI has the ability to provide workers’ compensation coverage to its clients. We provide this coverage through a variety of methods, all of which are subject to rigorous underwriting to assess financial stability, risk factors and cultural alignment related to safety and the client’s desire to improve their operations. In providing this coverage, we are responsible for complying with applicable statutory requirements for workers' compensation coverage.

Risk mitigation is also an important contributor to our principal goal of helping business owners operate their business more efficiently. It is in the mutual interests of the client and BBSI to commit to workplace safety and risk mitigation. We maintain clear guidelines for our area managers and risk management consultants, directly tying their continued employment to their diligence in understanding and addressing the risks of accident or injury associated with the industries in which client companies operate and in monitoring clients’ compliance with workplace safety requirements.

Elements of Workers' Compensation System

State law (and for certain types of employees, federal law) generally mandates that an employer reimburse its employees for the costs of medical care and other specified benefits for injuries or illnesses, including catastrophic injuries and fatalities, incurred in the course and scope of employment. Most states require employers to maintain workers' compensation insurance or otherwise demonstrate financial responsibility to meet workers' compensation obligations to employees. The benefits payable for various categories of claims are determined by state regulation and vary with the severity and nature of the injury or illness and other specified factors. In return for this guaranteed protection, workers' compensation is an exclusive remedy and employees are generally precluded from seeking other damages from their employer for workplace injuries. In many states, employers who meet certain financial and other requirements are permitted to self-insure.

Insurance Coverage for Workers' Compensation

The Company is a self-insured employer with respect to workers' compensation coverage for all of its employees (including employees co-employed through our client service agreements) working in Colorado, Maryland and Oregon. In the state of Washington, state law allows only the Company's staffing services and internal management employees to be covered under the Company's self-insured workers' compensation program. The Company also operates a wholly owned, fully licensed insurance company, Ecole, which provides workers’ compensation coverage to the Company’s employees working in Arizona and Utah.

For all other clients, the Company obtains policies from Chubb Limited (“Chubb”) through an arrangement known as a fronted program, which provides a licensed, admitted insurance carrier to issue policies on behalf of the Company. Chubb assumes credit risk should the Company be unable to satisfy its indemnification obligations.

Through various insurance arrangements, the Company retains risk of loss up to the first $5.0 million per occurrence, except in Maryland and Colorado, where our retention per occurrence is $1.0 million and $2.0 million, respectively.

6

As a result of our status as a self-insured employer in four states and our retention arrangements, our workers' compensation expense is tied directly to the incidence and severity of covered workplace injuries. We seek to contain our workers' compensation costs through a comprehensive approach to claims management. We use managed-care systems to reduce medical costs and keep time-loss costs to a minimum by assigning injured workers, whenever possible, to short-term assignments which accommodate the workers' physical limitations. We believe that these assignments minimize both time actually lost from work and covered time-loss costs. We engage a third-party claims administrator ("TPA") to provide the primary claims management expertise. Typical claims management procedures include performing thorough and prompt on-site investigations of claims filed by employees, working with physicians to encourage efficient medical management of cases, denying questionable claims and attempting to negotiate early settlements to eliminate future adverse development of claims costs. We also maintain a corporate-wide pre-employment drug screening program and a post-injury drug test program. We believe our claims management program has resulted in a reduction in the frequency of fraudulent claims and in accidents in which the use of illicit drugs appears to have been a contributing factor.

Employees and Employee Benefits

At December 31, 2019, we had 127,085 total employees, including 120,249 employees under our client service agreements, 6,035 staffing services employees, 796 managerial, sales and administrative employees (together, “management employees”), and 4 executive officers. The number of employees at any given time may vary significantly due to business conditions at customer or client companies. We believe our employee relations are good.

We offer various qualified employee benefit plans to our employees, including those employees for whom we are the administrative employer in a co-employment arrangement who so elect. Employees covered under a PEO arrangement may participate in our 401(k) plan at the sole discretion of the PEO client. Our qualified staffing and management employee benefit plans include our 401(k) plan, in which employees may enroll upon reaching 21 years of age and completing 1,000 hours of service in a 12 consecutive month period. We make matching contributions to the 401(k) plan under a safe harbor provision, which are immediately 100% vested. We match 100% of contributions by management and staffing employees up to 3% of each participating employee's annual compensation and 50% of the employee's contributions up to an additional 2% of annual compensation. We may also make discretionary contributions to the 401(k) plan, which vest over six years and are subject to certain legal limits, at the sole discretion of our Board of Directors.

We also offer a cafeteria plan under Section 125 of the Internal Revenue Code and group health, life insurance and disability insurance plans to qualified staffing and management employees. Generally, qualified employee benefit plans are subject to provisions of both the Internal Revenue Code and the Employee Retirement Income Security Act of 1974 ("ERISA"). In order to qualify for favorable tax treatment under the Internal Revenue Code, qualified plans must be established and maintained by an employer for the exclusive benefit of its employees.

Certain highly compensated employees of the Company are allowed to participate in a nonqualified deferred compensation plan. Under the plan, participants are permitted to defer receipt for income tax purposes of up to 90% of salary and up to 100% of any incentive bonus. Participants earn a return on their deferred compensation based on investment earnings of participant-selected investments. As an incentive to participate in the plan, the Company awards restricted stock units with a value equal to 35% of the amount deferred under the plan, up to a maximum of $75,000 per year. The restricted stock units vest in full on the fifth anniversary of the grant date, contingent on the continued employment of the participant.

The Company established a Rabbi trust under which compensation deferred by participants is deposited and held separately from the Company's other assets, subject to the claims of the Company's creditors in the event of its bankruptcy or insolvency.

7

The Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 (collectively, the “Acts”) subject us to potential penalties unless we offer to our employees minimum essential healthcare coverage that is affordable. Because each PEO client is considered to be the sole employer in the application of any rule or law included within the scope of the Acts, we do not offer health care coverage to the employees of our PEO clients. However, in order to comply with the employer mandate provision of the Acts, we offer health care coverage to all eligible staffing employees and management employees eligible for coverage under the Acts.

Regulatory and Legislative Issues

We are subject to the laws and regulations of the jurisdictions within which we operate, including those governing self-insured employers under the workers' compensation systems in Oregon, Maryland, and Colorado, as well as in Washington for staffing and management employees. We are also subject to laws and regulations governing our two wholly owned insurance companies in Arizona. While the specific laws and regulations vary among these jurisdictions, they typically require some form of licensing and often have statutory requirements for workplace safety and notice of change in obligation of workers’ compensation coverage in the event of contract termination. Although compliance with these requirements imposes some additional financial risk, particularly with respect to those clients who breach their payment obligation to us, such compliance has not had a material adverse effect on our business to date.

Our operations are affected by numerous federal and state laws relating to labor, tax and employment matters. Through our client services agreement, we assume certain obligations and responsibilities as the administrative employer under federal and state laws. Since many of these federal and state laws were enacted prior to the development of nontraditional employment relationships, such as professional employer, temporary employment, and outsourcing arrangements, many of these laws do not specifically address the obligations and responsibilities of nontraditional employers. In addition, the definition of "employer" under these laws is not uniform.

As an employer, we are subject to all federal statutes and regulations governing our employer-employee relationships. Subject to the discussion of risk factors below, we believe that our operations are in compliance in all material respects with applicable federal statutes and regulations.

Additional Information

Our filings with the SEC, including our annual report on Form 10-K, quarterly reports on Form 10-Q, periodic reports on Form 8-K and amendments to these reports, are accessible free of charge at our website at http://www.mybbsi.com as soon as reasonably practicable after they are electronically filed with the SEC. By making this reference to our website, we do not intend to incorporate into this report any information contained in the website. The website should not be considered part of this report.

Materials that the Company files with the SEC may be read and copied at the SEC’s Public Reference Room at 100 F Street, NE., Washington, DC 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-202-551-8090 or by e-mail at publicinfo@sec.gov. The SEC also maintains a website at http://www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers with publicly traded securities, including the Company.

8

In addition to other information contained in this report, the following risk factors should be considered carefully in evaluating our business.

Risks Relating to Our Business and Industry

Our consolidated retention for workers' compensation claims is $5.0 million per occurrence under our insurance arrangement with Chubb in the majority of states in which we operate.

We maintain our consolidated retention at $5.0 million per occurrence, except in Maryland and Colorado where our retention is at $1.0 million and $2.0 million per occurrence, respectively, due to regulatory requirements. The Company maintains its excess workers’ compensation insurance coverage with Chubb. Additionally, Ecole’s retention is at $5.0 million per occurrence for coverage in Arizona and Utah. Thus, the Company has financial risk for most workers' compensation claims under $5.0 million on a per occurrence basis. This level of per occurrence retention may result in higher workers’ compensation costs to us with a corresponding negative effect on our operating results and financial condition.

Our ability to continue our business operations under our present service model is dependent on maintaining workers' compensation insurance coverage.

Our arrangement with Chubb to provide workers’ compensation coverage to BBSI’s PEO clients extends through June 30, 2020, with the possibility of additional annual renewals. If Chubb is unwilling or unable to renew our arrangement in the future, we would need to seek alternative coverage. If replacement coverage were unavailable or available only on significantly less favorable terms, our business and results of operations would be materially adversely affected.

Collateral requirements could increase beyond our ability to satisfy those requirements.

The Company is required to provide collateral for its fronted program and by certain states related to its current and former status as a self-insured employer. Various factors, including adverse loss experience or a decline in the fair value of investments in our collateral accounts, could cause the counterparties to require that additional collateral be posted. To partially satisfy these collateral requirements, the Company has provided surety bonds and standby letters of credit. If there are significant changes to the market for these credit products, or if we are unable to renew these agreements, we may incur increased costs or be required to deposit additional capital as collateral.

Failure to manage the severity and frequency of workplace injuries will increase our workers’ compensation expenses.

Significant increases in the relative frequency or severity of workplace injuries due to failures to accurately assess potential risks or assure implementation of effective safety measures by our clients may result in increased workers’ compensation claims expenses, with a corresponding negative effect on our results of operations and financial condition.

9

Our investment portfolio is subject to market and credit risks, which could adversely impact our financial condition or results of operations.

We seek to hold a diversified portfolio of high-quality investments that is managed by a professional investment advisory firm in accordance with our investment policy and routinely reviewed by management and approved by our risk management committee. However, our investments are subject to general economic conditions and market risks as well as risks inherent to particular securities, including credit, interest rate and liquidity risks. Our portfolio consists primarily of debt securities and is subject to the risk that certain investments may default or become impaired due to deterioration in the financial condition of one or more issuers of the securities. Although our investment strategy is designed to preserve our capital, we cannot be certain that our investment objectives will be achieved, and we could incur substantial realized and unrealized investment losses in future periods.

We may be unable to draw on our revolving credit facility in the future.

If our business does not perform as expected, including if we generate less revenue than anticipated from our operations or encounter significant unexpected costs, we may fail to comply with the financial covenants under our credit facilities. If we do not comply with our financial covenants and we do not obtain a waiver or amendment from our lender, the lender may elect to cause all amounts owed to become immediately due and payable or may decline to renew our credit facility. In that event, we would seek to establish a replacement credit facility with one or more other lenders, including lenders with which we have an existing relationship, potentially on less desirable terms. There can be no guarantee that replacement financing would be available at commercially reasonable terms, if at all.

Our business is subject to risks associated with geographic market concentration.

Our California operations accounted for approximately 77% of our total revenues in 2019. As a result of the current importance of our California operations and anticipated continued growth from these operations, our profitability over the next several years is expected to be largely dependent on economic and regulatory conditions in California. If California experiences an economic downturn, or if the regulatory environment changes in a way that adversely affects our ability to do business or limits our competitive advantages, our profitability and growth prospects may be materially adversely affected. Similarly, due to our geographic concentration in California, a natural disaster or major event that disrupts these markets or the related workforce could have an immediate and material adverse impact on our operations and profitability.

In order to continue to grow revenues, we are dependent on retaining current clients and attracting new clients.

The Company’s revenue growth can be volatile and is dependent on same customer sales and the addition of new clients. Revenues increased 0.2% in 2019 and 2.2% in 2018. There can be no assurance that we will continue to grow revenues. Efforts to achieve business growth intensifies pressure on retaining current clients and attracting increasing numbers of new clients.

10

Economic conditions, particularly in California, may impact our ability to attract new clients and cause our existing clients to reduce staffing levels or cease operations.

Weak economic conditions typically have a negative impact on small-and mid-sized businesses, which make up the majority of our clients. In turn, these businesses could cut costs, including trimming employees from their payrolls, or closing locations or ceasing operations altogether. If weak economic conditions were to develop, these forces may result in decreased revenues due both to the downsizing of our current clients and increased difficulties in attracting new clients in a poor economic environment. In addition, weak economic conditions may also result in additional bad debt expense to the extent that existing clients cease operations.

Our business is subject to risks associated with healthcare reforms.

The Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 (collectively, the “Acts”) subject us to potential penalties unless we offer our employees minimum essential healthcare coverage that is affordable. In order to comply with the employer mandate provision of the Acts, we offer health care coverage to all temporary and permanent employees eligible for coverage under the Acts other than employees of our PEO clients, which are responsible for providing required health care coverage to their employees. Designating employees as eligible is complex and is subject to challenge by employees and the Internal Revenue Service (“IRS”). While we believe we have properly identified eligible employees, a later determination that we failed to offer the required health coverage to eligible employees could result in penalties that may materially harm our business. We cannot be certain that compliant insurance coverage will remain available to us on reasonable terms, and we could face additional risks arising from future changes to or repeal of the Acts or changed interpretations of our obligations under the Acts. There can be no assurance that we will be able to recover all related costs through increased pricing to our customers or that such costs will be recovered in the period in which costs are incurred, and the net financial impact on our results of operations could be significant.

Changes in our income tax positions or adverse outcomes resulting from on-going or future tax audits could harm our business, operating results, financial condition and prospects.

Significant judgments and estimates are required in determining our provision for income taxes and other tax liabilities. In determining the adequacy of our tax provision, we assess the likelihood of adverse outcomes that could result if our tax positions were challenged by the IRS and other tax authorities. The tax authorities in the U.S. regularly examine our income and other tax returns. The ultimate outcome of tax examinations and disputes cannot be predicted with certainty. Should the IRS or other tax authorities assess additional taxes as a result of these or other examinations, we may be required to record charges to operations that could have a material impact on our results of operations, financial position or cash flows.

If we are unable to maintain our brand image and corporate reputation, our business may suffer.

Our success depends in part on our ability to maintain our reputation for providing excellent service to our customers. Service quality issues, whether actual or perceived, and even when false or unfounded, could tarnish the image of our brand and may cause customers to use other companies. Also, adverse publicity surrounding labor relations, data breaches, SEC investigations, securities class actions and the like, could negatively affect our overall reputation. Damage to our reputation could reduce demand for our services and thus have an adverse effect on our business, financial condition and results of operations.

11

Our staffing business is vulnerable to economic fluctuations.

Demand for our staffing services is sensitive to changes in the level of economic activity in the regions in which we do business. As economic activity slows down, companies often reduce their use of temporary employees before undertaking layoffs of permanent staff, resulting in decreased demand for staffing services. During strong economic periods, on the other hand, we often experience shortages of qualified employees to meet customer needs, as occurred during 2019.

Because we assume the obligation to make wage, tax and regulatory payments in respect of some employees, we are exposed to client credit risks.

We generally assume credit risk associated with our clients’ employee payroll obligations, including liability for payment of salaries and wages (including payroll taxes), as well as retirement benefits. These obligations are fixed whether or not the client makes payments to us as required by our services agreement. We attempt to mitigate this risk by invoicing our clients at the end of their specific payroll processing cycle. We also carefully monitor the timeliness of our clients' payments and impose strict credit standards on our customers. If we fail to successfully manage our credit risk, our results of operations and financial condition could be materially and adversely affected.

Increases in unemployment claims could raise our state and federal unemployment tax rates which we may not be able to pass on to our customers.

During weak economic conditions in our markets, the level of unemployment claims tends to rise as a result of employee layoffs at our clients and lack of work in our temporary staffing pool. The rise in unemployment claims often results in higher state and federal unemployment tax rates, which in most instances cannot be concurrently passed on to our customers either due to existing client services agreements or competitive pricing pressures. Increases in our state and federal unemployment tax rates could have a material adverse effect on our results of operations, particularly in the early part of the calendar year when payroll tax rates are at or near their maximum.

If we are determined not to be an “employer” under certain laws and regulations, our clients may stop using our services, and we may be subject to additional liabilities.

We are the administrative employer in our co-employment relationships under the various laws and regulations of the IRS and the U.S. Department of Labor. If we are determined not to be the administrative employer under such laws and regulations and are therefore unable to assume our clients’ obligations for employment and other taxes, our clients may be held jointly and severally liable for payment of such taxes. Some clients or prospective clients may view such potential liability as an unacceptable risk, discouraging current clients from continuing a relationship with us or prospective clients from entering into a new relationship with us. Any determination that we are not the administrative employer for purposes of ERISA could also adversely affect our cafeteria benefits plan operated under Section 125 of the Internal Revenue Code and result in liabilities to us under the plan.

12

We may be exposed to employment‑related claims and costs and periodic litigation that could adversely affect our business and results of operations.

We either co-employ employees in connection with our PEO client services agreements or place our employees in our customers' workplace in connection with our staffing business. As such, we are subject to a number of risks inherent to our status as the administrative employer, including without limitation:

|

|

• |

claims of misconduct or negligence on the part of our employees, discrimination or harassment claims against our employees, or claims by our employees of discrimination or harassment by our clients; |

|

|

• |

immigration-related claims; |

|

|

• |

claims relating to violations of wage, hour and other workplace regulations; |

|

|

• |

claims relating to employee benefits, entitlements to employee benefits, or errors in the calculation or administration of such benefits; and |

|

|

• |

possible claims relating to misuse of customer confidential information, misappropriation of assets or other similar claims. |

If we experience significant incidents involving any of the above-described risk areas, we could face substantial out-of-pocket losses, fines or negative publicity. In addition, such claims may give rise to litigation, which may be time consuming, distracting and costly, and could have a material adverse effect on our business. With respect to claims involving our co-employer relationships, although our client services agreement provides that the client will indemnify us for any liability attributable to the conduct of the client or its employees, we may not be able to enforce such contractual indemnification, or the client may not have sufficient assets to satisfy its obligations to us. An increase in employment-related claims against us may have a material adverse effect on our results of operations.

We are dependent upon technology services, and if we experience damage, service interruptions or failures in our computer and telecommunications systems, our client relationships and our ability to attract new clients may be adversely affected.

We rely extensively on computer systems to provide service offerings to our clients, manage our branch network, perform employment-related services and accounting and reporting functions, and summarize and analyze our financial results. Our systems are subject to damage or interruption from telecommunications failures, power-related outages, third-party disruptions, computer viruses and malicious attacks, security breaches and catastrophic events. If our systems are damaged or fail to function properly, we may incur substantial costs to repair or replace them, experience loss of critical data and interruptions or delays in our ability to manage our operations, and encounter a loss of client confidence. In addition, our clients’ businesses may be adversely affected by any system or equipment failure or breach we experience. As a result, we may suffer damage to our reputation, we may lose clients, our ability to attract new clients may be adversely affected, and we could be exposed to contractual liability.

We depend on third-party software in order to provide our services and support our operations.

Significant portions of our services and operations rely on software that is licensed from third-party vendors. The fees associated with these license agreements could increase in future periods, resulting in increased operating expenses. If there are significant changes to the terms and conditions of our license agreements, or if we are unable to renew these license agreements, we may be required to make changes to our vendors or information technology systems. These changes may impact the services we provide to our clients or the processes we have in place to support our operations, which could have an adverse effect on our business.

13

We could be subject to reduced revenues, increased costs, liability claims, or harm to our reputation as a result of data theft, cyberattacks or other security vulnerabilities.

The nature of our business involves the receipt, storage, and transmission of personal and proprietary information about thousands of employees and clients. Attacks on information technology systems continue to grow in frequency and sophistication, and we and our third-party vendors are targeted by unauthorized parties using malicious tactics, code and viruses. Hardware or applications we develop or procure from third-party vendors may contain defects in design or other problems that could unexpectedly compromise the confidentiality, integrity or availability of data or our systems. Because the techniques used to obtain unauthorized access and disable or sabotage systems change frequently and may be difficult to detect for long periods of time, we and our third-party vendors may be unable to anticipate these techniques or implement adequate preventive measures. As these threats continue to evolve, we may be required to invest significant additional resources to modify and enhance our information security and controls or to investigate and remediate any security vulnerabilities. While our technology infrastructure is designed to safeguard and protect personal and business information, we have limited ability to monitor the implementation of similar safeguards by our vendors.

Any cyberattack, unauthorized intrusion, malicious software infiltration, network disruption, corruption of data, misuse or theft of private or other sensitive information, or inadvertent acts by our own employees, could result in the disclosure or misuse of confidential or proprietary information, which could have a material adverse effect on our business operations or that of our clients. If we experience a significant data security breach or fail to detect and appropriately respond to a significant data security breach, we could be exposed to government enforcement actions and private litigation. These losses may exceed our insurance coverage for such incidents. In addition, our employees and clients could lose confidence in our ability to protect their personal and proprietary information, which could cause them to terminate their relationships with us. Any loss of confidence arising from a significant data security breach could hurt our reputation, further damaging our business.

We operate in a complex regulatory environment, and failure to comply with applicable laws and regulations could adversely affect our business.

Corporate human resource operations are subject to a broad range of complex and evolving laws and regulations, including those applicable to payroll practices, benefits administration, employment practices, workers’ compensation coverage, and privacy. Because our clients have employees in many states throughout the United States, we must perform our services in compliance with the legal and regulatory requirements of multiple jurisdictions. Some of these laws and regulations may be difficult to ascertain or interpret and may change from time to time. Violation of such laws and regulations could subject us to fines and penalties, damage our reputation, constitute a breach of our client agreements, impair our ability to obtain and renew required licenses, and decrease our profitability or competitiveness. If any of these effects were to occur, our operating results and financial condition could be adversely affected.

14

Changes in government regulations may result in restrictions or prohibitions applicable to the provision of employment services or the imposition of additional licensing, regulatory or tax requirements.

Our business is heavily regulated in most jurisdictions in which we operate. We cannot provide assurance that the states in which we conduct or seek to conduct business will not:

|

|

• |

impose additional regulations that prohibit or restrict employment-related businesses like ours; |

|

|

• |

require additional licensing or add restrictions on existing licenses to provide employment-related services; or |

|

|

• |

increase taxes or make changes in the way in which taxes are calculated for providers of employment-related services. |

Any changes in applicable laws and regulations may make it more difficult or expensive for us to do business, inhibit expansion of our business, or result in additional expenses that limit our profitability or decrease our ability to attract and retain clients.

The tax status of our insurance subsidiaries could be challenged by taxing authorities resulting in increased or accelerated income tax payments.

In conjunction with our workers’ compensation program, we operate two wholly owned insurance subsidiaries, Associated Insurance Company for Excess (“AICE”) and Ecole. We treat the two subsidiaries as insurance companies for federal and state income tax purposes. If the IRS or a state taxing authority were to determine that the subsidiaries do not qualify as insurance companies, in which insurance reserves are currently deductible, we could be subject to additional taxation or required to make accelerated income tax payments that we otherwise would have deferred until future periods.

Our wholly owned insurance companies are subject to substantial government regulation.

Our wholly owned insurance companies are primarily regulated by state insurance commissioners. Such regulation includes monitoring the financial status of these companies, approving policies and premium rates, maintaining requirements for capital surplus and types of investments, and approving any significant changes to the legal or operating structure of these entities. State regulators can also impose taxes and other fees on insurance companies under their jurisdiction. These regulations may restrict our ability to operate these companies in the manner we believe is best, which could increase the cost of our operations, restrict our access to insurance coverage or adversely affect our liquidity.

We may find it difficult to expand our business into additional states due to varying state regulatory requirements.

Future growth in our operations depends, in part, on our ability to offer our services to prospective clients in new states, which may subject us to different regulatory requirements and standards. In order to operate effectively in a new state, we must obtain all necessary regulatory approvals, adapt our procedures to that state's regulatory requirements and modify our service offerings to adapt to local market conditions. As we expand into additional states, we may not be able to duplicate in other markets the financial performance experienced in our current markets.

15

We face competition from a number of other companies.

We face competition from various companies that may provide all or some of the services we offer. Our competitors include companies that are engaged in staffing services such as Robert Half International Inc., Kelly Services, Inc., and ManpowerGroup Inc.; companies that are focused on co-employment, such as Insperity, Inc., and TriNet Group, Inc.; and companies that primarily provide payroll processing services, such as Automatic Data Processing, Inc. and Paychex, Inc. We also face competition from information technology outsourcing firms and broad-based outsourcing and consulting firms that perform individual projects.

Several of our existing or potential competitors have substantially greater financial, technical and marketing resources than we do, which may enable them to:

|

|

• |

develop and expand their infrastructure and service offerings more quickly and achieve greater cost efficiencies; |

|

|

• |

invest in new technologies; |

|

|

• |

expand operations into new markets more rapidly; |

|

|

• |

devote greater resources to marketing; |

|

|

• |

compete for acquisitions more effectively and complete acquisitions more easily; and |

|

|

• |

aggressively price products and services and increase benefits in ways that we may not be able to match financially. |

In order to compete effectively in our markets, we must target our potential clients carefully, continue to improve our efficiencies and the scope and quality of our services, and rely on our service quality, innovation, education and program clarity. If our competitive advantages are not compelling or sustainable, then we are unlikely to increase or sustain profits and our stock price could decline.

To succeed, we must constantly improve our technology to meet the expectations of our clients. If we fail to meet those expectations, we may lose clients and harm our business.

In order to attract and retain clients and satisfy their expectations, the software, hardware and networking technologies we use must be frequently and rapidly upgraded, enhanced and improved in response to technological advances, competitive pressures, client expectations, and new and changing laws. Failure to successfully implement technological improvements could result in harm to our reputation, loss of market share, reduced revenue, or client claims against us, any of which could materially harm our business.

As we continue to invest in upgrades or replacements to our existing systems, including enhancements and additional security measures, we may incur substantial costs and risks relating to development, installation and implementation, including disruptions in our service offerings or increases in expected costs, which may have a material adverse effect on our operating results and financial condition.

We are dependent upon certain key personnel and recruitment and retention of key employees may be difficult and expensive.

We believe that the successful operation of our business is dependent upon our retention of the services of key personnel, including our Chief Executive Officer, other executive officers and area managers. We may not be able to retain all of our executives, senior managers and key personnel in light of competition for their services. If we lose the services of one of our executive officers or a significant number of our senior managers, our results of operations likely would be adversely affected.

16

We do not have an expansive in-house sales staff and therefore rely extensively on referral partners.

We maintain a minimal internal professional sales force, and we rely heavily on referral partners to provide referrals to new business. In connection with these arrangements, we pay a fee to referral partners for new clients. These referral firms and individuals do not have an exclusive relationship with us. If we are unable to maintain these relationships or if they increase their fees or lose confidence in our services, we could face declines in our business and additional costs and uncertainties as we attempt to hire and train an internal sales force.

We depend on attracting and retaining qualified employees; during periods of economic growth, our costs to do so increase and attracting and retaining people becomes more difficult.

Our teams of client-facing professionals are the foundation of our value proposition. Our ability to attract and retain qualified personnel could be impaired by economic conditions resulting in lower unemployment and increases in compensation. During periods of economic growth, we face increased competition for retaining and recruiting qualified personnel, which in turn leads to greater advertising and recruiting costs and increased salary expenses. If we cannot attract and retain qualified employees, the quality of our services may deteriorate and our reputation and results of operations could be adversely affected.

Our service agreements may be terminated on short notice, leaving us vulnerable to a significant loss of customers in a short period of time, if business or regulatory conditions change or events occur that negatively affect our reputation.

Our client services agreements are generally terminable on 30 days’ notice by either us or our client. As a result, our clients may terminate their agreement with us at any time, making us particularly vulnerable to changing business or regulatory conditions or changes affecting our reputation or the reputation of our industry.

Changes in federal and state unemployment tax laws and regulations could adversely affect our business.

In past years, there has been significant negative publicity relating to the use of staffing or PEO companies to shield employers from poor unemployment history and high unemployment taxes. New legislation enacted at the state or federal level to try to counter this perceived problem could have a material adverse effect on our business by limiting our ability to market our services or making our services less attractive to our customers and potential customers.

17

Risks Related to Ownership of our Common Stock

Our stock price may be volatile or may decline, resulting in substantial losses for our stockholders.

The market price of our Common Stock has been, and may continue to be, volatile for the foreseeable future. Important factors that may cause our trading price to decline include the factors listed below and other factors that may have a material adverse effect on our business or financial results, including those described above in this “Risk Factors” section:

|

|

• |

actual or anticipated fluctuations in our results of operations, including a significant slowdown in our revenue growth or material increase in our workers’ compensation expense; |

|

|

• |

our failure to maintain effective internal control over financial reporting or otherwise discover material errors in our financial reporting; |

|

|

• |

imposition of significant fines or penalties or other adverse action by regulatory authorities against the Company; |

|

|

• |

adverse developments in legal proceedings involving claims against the Company; |

|

|

• |

our failure to meet financial projections or achieve financial results anticipated by analysts; or |

|

|

• |

changes in our board of directors or management. |

Maryland law and our Charter and bylaws contain provisions that could make the takeover of the Company more difficult.

Certain provisions of Maryland law and our Charter and bylaws could have the effect of delaying or preventing a third party from acquiring the Company, even if a change in control would be beneficial to our stockholders. These provisions of our Charter and bylaws permit the Board of Directors to issue up to 500,000 shares of preferred stock with such rights and preferences, including voting rights, as the Board may establish, without further approval by the Company's stockholders, which could also adversely affect the voting power of holders of our Common Stock.

In addition, the Company is subject to the Maryland control share act (the “Control Share Act”). Under the Control Share Act, a person (an “Acquiring Person”) who acquires voting stock in a transaction (a “Control Share Acquisition”) which results in its holding voting power within specified ranges cannot vote the shares it acquires in the Control Share Acquisition unless voting rights are accorded to such control shares by the holders of two-thirds of the outstanding voting shares, excluding the Acquiring Person and the Company's officers and directors who are also employees of the Company.

The Company is also subject to the provisions of Maryland law limiting the ability of certain Maryland corporations to engage in specified business combinations (the “Business Combination Act”). Subject to certain exceptions, the Business Combination Act prohibits a Maryland corporation from engaging in a business combination with a stockholder who, with its affiliates, owns 10% or more of the corporation's voting stock. These provisions will not apply to business combinations that are approved by the Board of Directors before the stockholder became an interested stockholder.

None.

18

We operate through 64 branch offices. The following table shows the number of locations in each state in which we have offices. We also lease office space in other locations in our market areas which we use to recruit and place employees.

|

|

|

Number of Branch |

|

Offices |

|

Locations |

|

California |

|

25 |

|

Oregon |

|

11 |

|

Utah |

|

5 |

|

Washington |

|

5 |

|

Colorado |

|

3 |

|

Idaho |

|

3 |

|

Arizona |

|

2 |

|

Maryland |

|

2 |

|

North Carolina |

|

2 |

|

Nevada |

|

2 |

|

Pennsylvania |

|

2 |

|

Delaware |

|

1 |

|

Virginia |

|

1 |

We lease office space for our branch offices. At December 31, 2019, our leases had expiration dates ranging from less than one year to seven years. Our corporate headquarters occupies approximately 73 percent of the 65,300 square foot building we own in Vancouver, Washington.

BBSI is not subject to material legal proceedings and claims other than those which arise in the ordinary course of our business, except for those matters discussed in “Note 12 - Litigation” to the consolidated financial statements incorporated into Item 8 of Part II of this report.

Not Applicable

|

Item 5. |

MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Our common stock (the "Common Stock") trades on the Global Select Market segment of The Nasdaq Stock Market under the symbol "BBSI." At February 10, 2020, there were 26 stockholders of record and approximately 3,879 beneficial owners of the Common Stock.

The Company maintains a stock repurchase program approved by the Board of Directors, which authorizes the repurchase of shares from time to time in open market purchases. On August 6, 2019, the Board of Directors authorized the repurchase of up to $50 million of the Company's common stock over a three-year period beginning August 15, 2019. No repurchases were made during the year ended December 31, 2019.

19

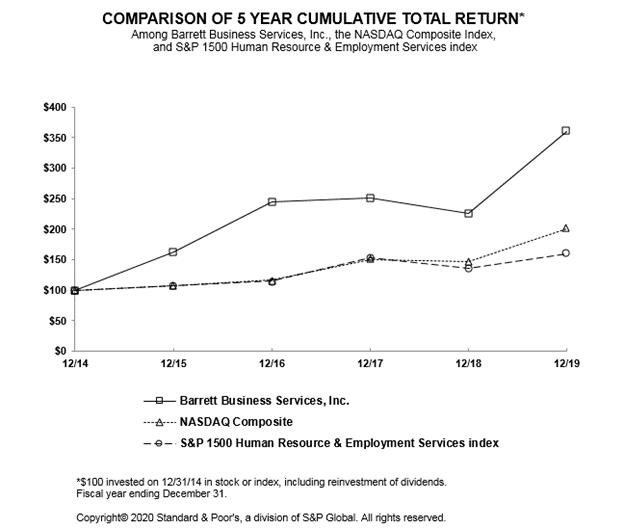

The following graph shows the cumulative total return at the dates indicated for the period from December 31, 2014 until December 31, 2019, for our Common Stock, The Nasdaq Composite Index, and the S&P 1500 Human Resource & Employment Services Index, a published industry index that is considered reflective of the Company’s peers.

The stock performance graph has been prepared assuming that $100 was invested on December 31, 2014 in our Common Stock and the indexes shown, and that dividends are reinvested. The stock price performance reflected in the graph may not be indicative of future price performance.

|

|

|

12/14 |

|

12/15 |

|

12/16 |

|

12/17 |

|

12/18 |

|

12/19 |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Barrett Business Services, Inc. |

|

|

100.00 |

|

|

162.59 |

|

|

244.87 |

|

|

250.64 |

|

|

225.35 |

|

|

360.78 |

|

|

NASDAQ Composite |

|

|

100.00 |

|

|

106.96 |

|

|

116.45 |

|

|

150.96 |

|

|

146.67 |

|

|

200.49 |

|

|

S&P 1500 Human Resource & Employment Services index |

|

|

100.00 |

|

|

107.33 |

|

|

114.70 |

|

|

153.24 |

|

|

135.54 |

|

|

160.06 |

|

20

The following selected consolidated financial data should be read in conjunction with the Company's consolidated financial statements and the accompanying notes in Item 8 of Part II, “Financial Statements and Supplementary Data,” and the information contained in Item 7 of Part II, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Historical results are not necessarily indicative of future results.

|

|

|

Year Ended December 31, |

|

|||||||||||||||||

|

|

|

2019 |

|

|

2018 |

|

|

2017 |

|

|

2016 |

|

|

2015 |

|

|||||

|

(In thousands, except per share data) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statement of operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenues: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Professional employer service fees |

|

$ |

819,873 |

|

|

$ |

793,399 |

|

|

$ |

758,046 |

|

|

$ |

673,924 |

|

|

$ |

572,286 |

|

|

Staffing services |

|

$ |

122,438 |

|

|

|

147,299 |

|

|

|

162,386 |

|

|

|

166,662 |

|

|

|

168,555 |

|

|

Total revenues |

|

|

942,311 |

|

|

|

940,698 |

|

|

|

920,432 |

|

|

|

840,586 |

|

|

|

740,841 |

|

|

Cost of revenues: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Direct payroll costs |

|

|

92,455 |

|

|

|

111,443 |

|

|

|

122,533 |

|

|

|

126,753 |

|

|

|

127,964 |

|

|

Payroll taxes and benefits |

|

|

429,713 |

|

|

|

407,003 |

|

|

|

404,687 |

|

|

|

357,867 |

|

|

|

312,284 |

|

|

Workers' compensation |

|

|

211,890 |

|

|

|

235,579 |

|

|

|

234,681 |

|

|

|

210,430 |

|

|

|

171,137 |

|

|

Total cost of revenues |

|

|

734,058 |

|

|

|

754,025 |

|

|

|

761,901 |

|

|

|

695,050 |

|

|

|

611,385 |

|

|

Gross margin |

|

|

208,253 |

|

|

|

186,673 |

|

|

|

158,531 |

|

|

|

145,536 |

|

|

|

129,456 |

|

|

Selling, general and administrative expenses |

|

|

153,879 |

|

|

|

145,465 |

|

|

|

123,138 |

|

|

|

113,342 |

|

|

|

90,177 |

|

|

Depreciation and amortization |

|

|

3,886 |

|

|

|

4,219 |

|

|

|

5,452 |

|

|

|

3,253 |

|

|

|

2,851 |

|

|

Income from operations |

|

|

50,488 |

|

|

|

36,989 |

|

|

|

29,941 |

|

|

|

28,941 |

|

|

|

36,428 |

|

|

Other income (expense): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment income, net |

|

|

12,520 |

|

|

|

9,077 |

|

|

|

4,668 |

|

|

|

956 |

|

|

|

771 |

|

|

Interest expense |

|

|

(1,789 |

) |

|

|

(1,052 |

) |

|

|

(313 |

) |

|

|

(807 |

) |

|

|

(1,965 |

) |

|

Loss on litigation |

|

— |

|

|

— |

|

|

— |

|

|

|

(3,544 |

) |

|

— |

|

||||

|

Other, net |

|

|

(81 |

) |

|

|

(245 |

) |

|

|

82 |

|

|

|

40 |

|

|

|

(88 |

) |

|

Other income (expense), net |

|

|

10,650 |

|

|

|

7,780 |

|

|

|

4,437 |

|

|

|

(3,355 |

) |

|

|

(1,282 |

) |

|

Income before income taxes |

|

|

61,138 |

|

|

|

44,769 |

|

|

|

34,378 |

|

|

|

25,586 |

|

|

|

35,146 |

|

|

Provision for income taxes |

|

|

12,846 |

|

|

|

6,707 |

|

|

|

9,208 |

|

|

|

6,787 |

|

|

|

9,652 |

|

|

Net income |

|

$ |

48,292 |

|

|

$ |

38,062 |

|

|

$ |

25,170 |

|

|

$ |

18,799 |

|

|

$ |

25,494 |

|

|

Basic income per common share |

|

$ |

6.48 |

|

|

$ |

5.18 |

|

|

$ |

3.46 |

|

|

$ |

2.60 |

|

|

$ |

3.55 |

|

|

Weighted average number of basic common shares outstanding |

|

|

7,451 |

|

|

|

7,342 |

|

|

|

7,275 |

|

|

|

7,226 |

|

|

|

7,173 |

|

|

Diluted income per common share |

|

$ |

6.27 |

|

|

$ |

4.98 |

|

|

$ |

3.33 |

|

|

$ |

2.55 |

|

|

$ |

3.47 |

|

|

Weighted average number of diluted common shares outstanding |

|

|

7,699 |

|

|

|

7,647 |

|

|

|

7,551 |

|

|

|

7,378 |

|

|

|

7,353 |

|

|

Cash dividends per common share |

|

$ |

1.10 |

|

|

$ |

1.00 |

|

|

$ |

1.00 |

|

|

$ |

0.88 |

|

|

$ |

0.88 |

|

|

Selected balance sheet data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

$ |

44,570 |

|

|

$ |

35,371 |

|

|

$ |

59,835 |

|

|

$ |

50,768 |

|

|

$ |

25,218 |

|

|

Investments |

|

|

82,590 |

|

|

|

2,103 |

|

|

|

1,873 |

|

|

|

6,317 |

|

|

|

6,082 |

|

|

Current assets |

|

|

423,848 |

|

|

|

321,673 |

|

|

|

308,235 |

|

|

|

235,383 |

|

|

|

206,068 |

|

|

Current liabilities |

|

|

342,122 |

|

|

|

326,738 |

|

|

|

322,255 |

|

|

|

275,164 |

|

|

|

237,393 |

|

|

Working capital surplus (deficit) |

|

|

81,726 |

|

|

|

(5,065 |

) |

|